Forty years ago, Gorbachev took over – Why did socialism collapse?

11 March 2025

On 11 March 1985, Mikhail Gorbachev was elected General Secretary of the Communist Party of the Soviet Union. He set in motion political and economic reforms that would change the world. What have been the economic reasons for the demise of communism?

image credit: Commons RIA Novosti archive / Yuryi Abramochkin

In this article, we explore why the socialist systems in Eastern Europe collapsed around 1990, drawing on our newly digitised wiiw COMECON [1] Dataset. We revisit traditional explanations framed as the ‘jockey’ (policy decisions), the ‘horse’ (inherent systemic flaws) and the ‘racetrack’ (external environment), concluding that the collapse resulted from the interplay of all three factors. If any one of these factors had been different, socialism might well have survived.

The collapse of socialism in Eastern Europe remains one of the most significant geopolitical shifts of the 20th century. While numerous studies and books have already examined the issue, our recent report ‘The jockey, horse and racetrack revisited: Why did CESEE’s command economies collapse?’[2] revisits the question, drawing on our newly released wiiw COMECON Dataset and reports that the wiiw was publishing at the time, trying to provide some fresh insights. This article highlights some of the key findings from the study.

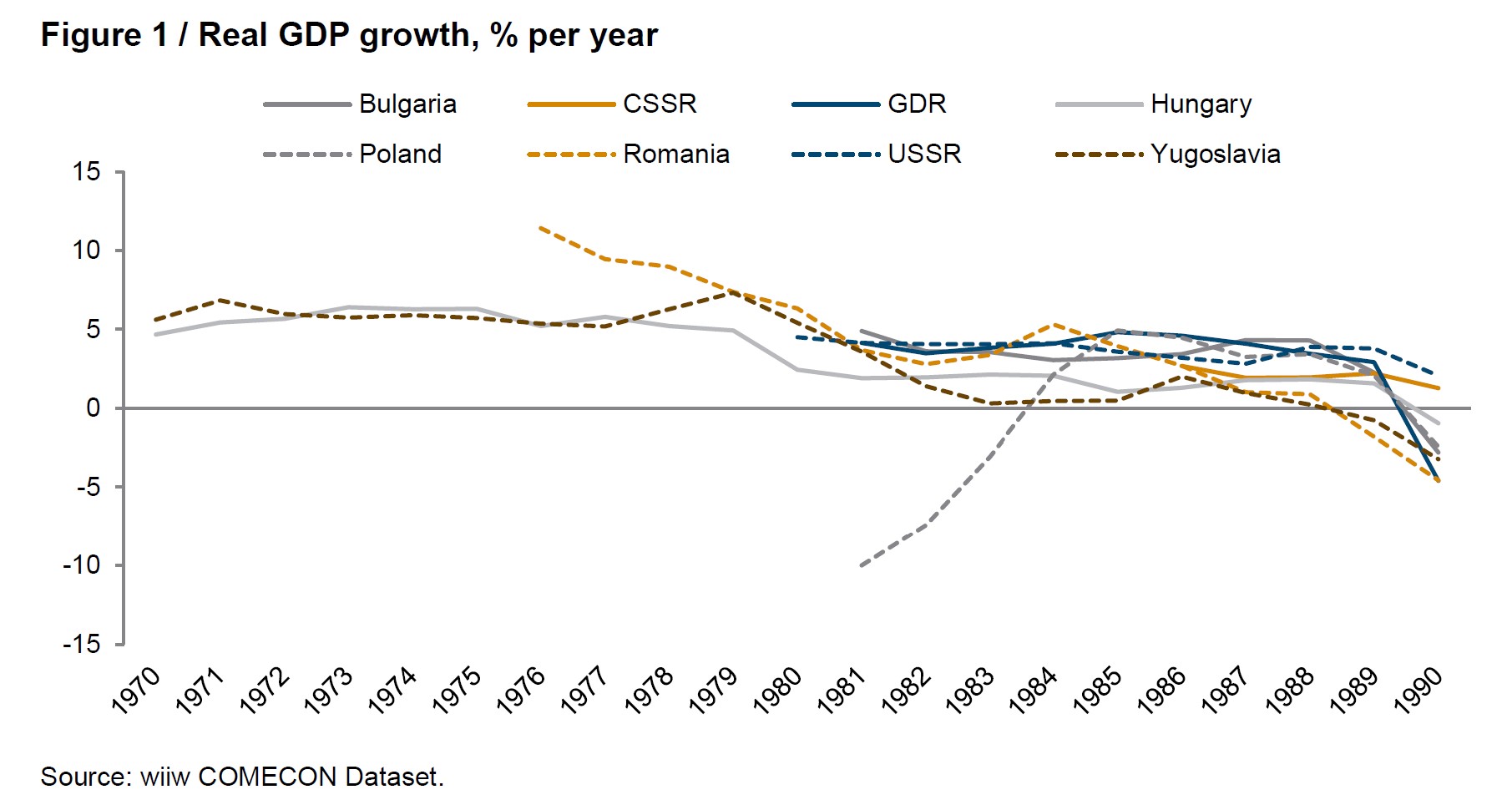

Solid growth until 1980 but slowdown afterwards, owing to weak investment

As the 1980s approached, the challenges faced by the socialist economies were becoming increasingly apparent, though the situation was not entirely bleak. Until 1980, growth consistently exceeded 5% in the countries with available data, but a notable slowdown began to emerge around this period (Figure 1). In Romania, the slowdown started earlier but from a relatively higher base. Poland’s experience stands out – the economy suffered sharply negative growth in the early 1980s before returning to positive territory by 1984. Interestingly, the first oil shock of 1973 had a relatively limited impact on growth in these economies, unlike in Western Europe. This was due to the favourable oil pricing policy the Soviet Union employed in its trade with these countries at the time. However, this policy was changed in 1975, leading to significant problems in the years that followed (a topic explored in more detail later in this article).

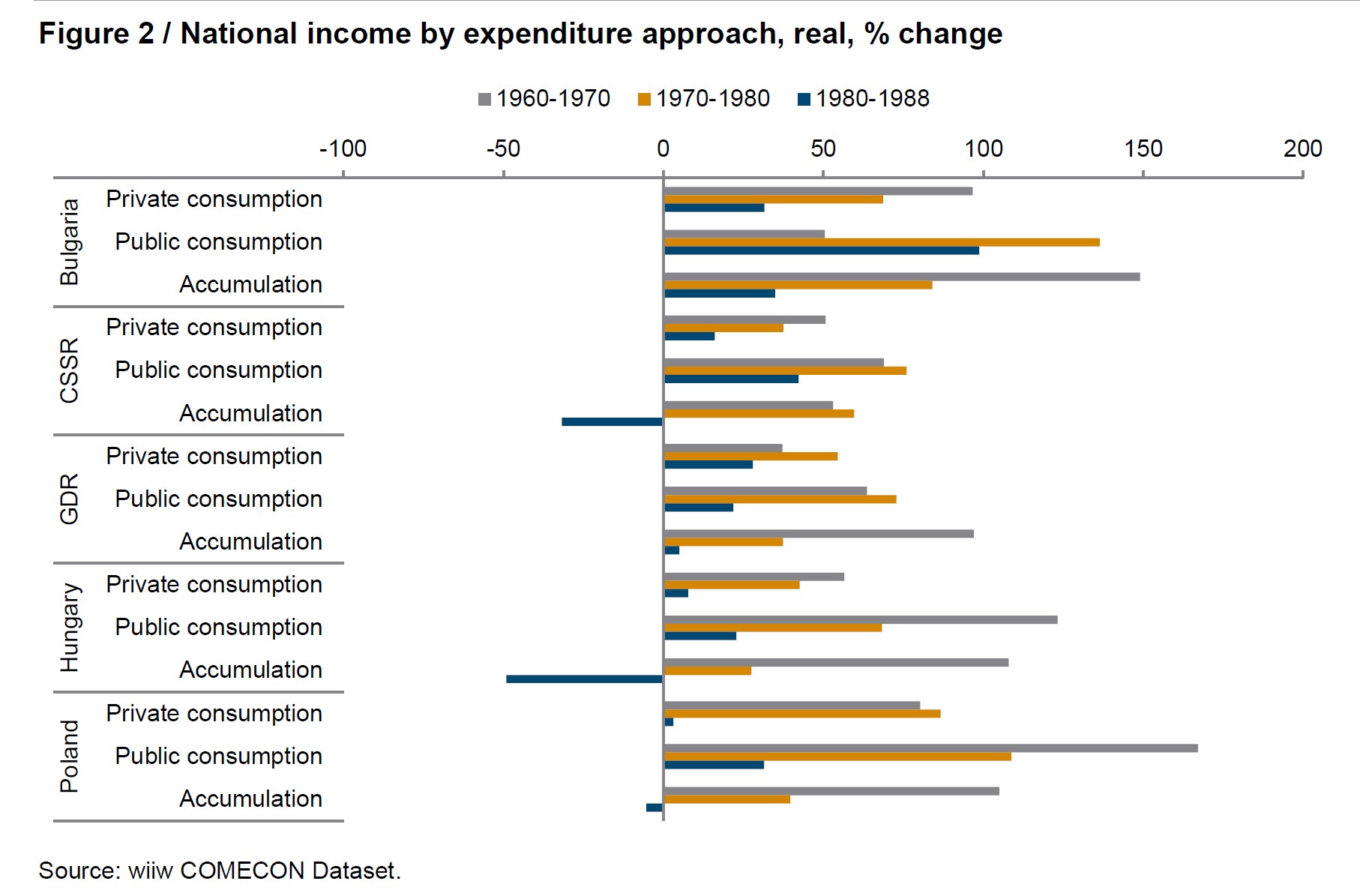

Examining available data on national income through the expenditure approach, which breaks national income into public consumption, private consumption and accumulation, provides valuable insights into most COMECON countries from the 1960s onward. The general trend shows that real growth was exceptionally strong across all major expenditure components during the 1960s. It remained solid, though already decelerating in many cases, throughout the 1970s, before slowing significantly or even turning negative during the 1980s (Figure 2). The primary cause of this slowdown was the consistent decline in accumulation growth – comprising investment and stock accumulation – across all countries during this period. In the CSSR, Hungary, and Poland, accumulation growth even turned negative in the 1980s. This indicates that the main driver of the economic decline in COMECON countries during the 1980s was the sustained lack of investment.

An unfavourable global environment in the 1970s and 1980s

The first explanation for the collapse of socialism is that it happened due to the unfavourable global environment, shaped by the oil shocks and rising global interest rates. The 1973-74 oil price shock indeed marked a turning point for the COMECON countries, as it led the Soviet Union to change its long- standing oil pricing policy. Prior to the shock, the USSR sold oil to COMECON countries at fixed prices, set for five years and typically well below market levels. In 1975, this was replaced with a pricing system based on a five-year moving average of global oil prices, adjusted annually. This extended the pain of the 1973-73 oil shock for COMECON economies well after the shocks were over.

Then when the 1979 oil shock came, accompanied by the rising global interest rates, the situation worsened further. A balance of payments crisis emerged everywhere in Eastern Europe, prompting severe austerity measures and a collapse in aggregate demand. The sharp decline in investment from 1980 mentioned before can largely be attributed to these events. The oil price hikes rendered many industries uncompetitive, while high Western interest rates made it increasingly difficult to finance the external debt accumulated during the 1970s.

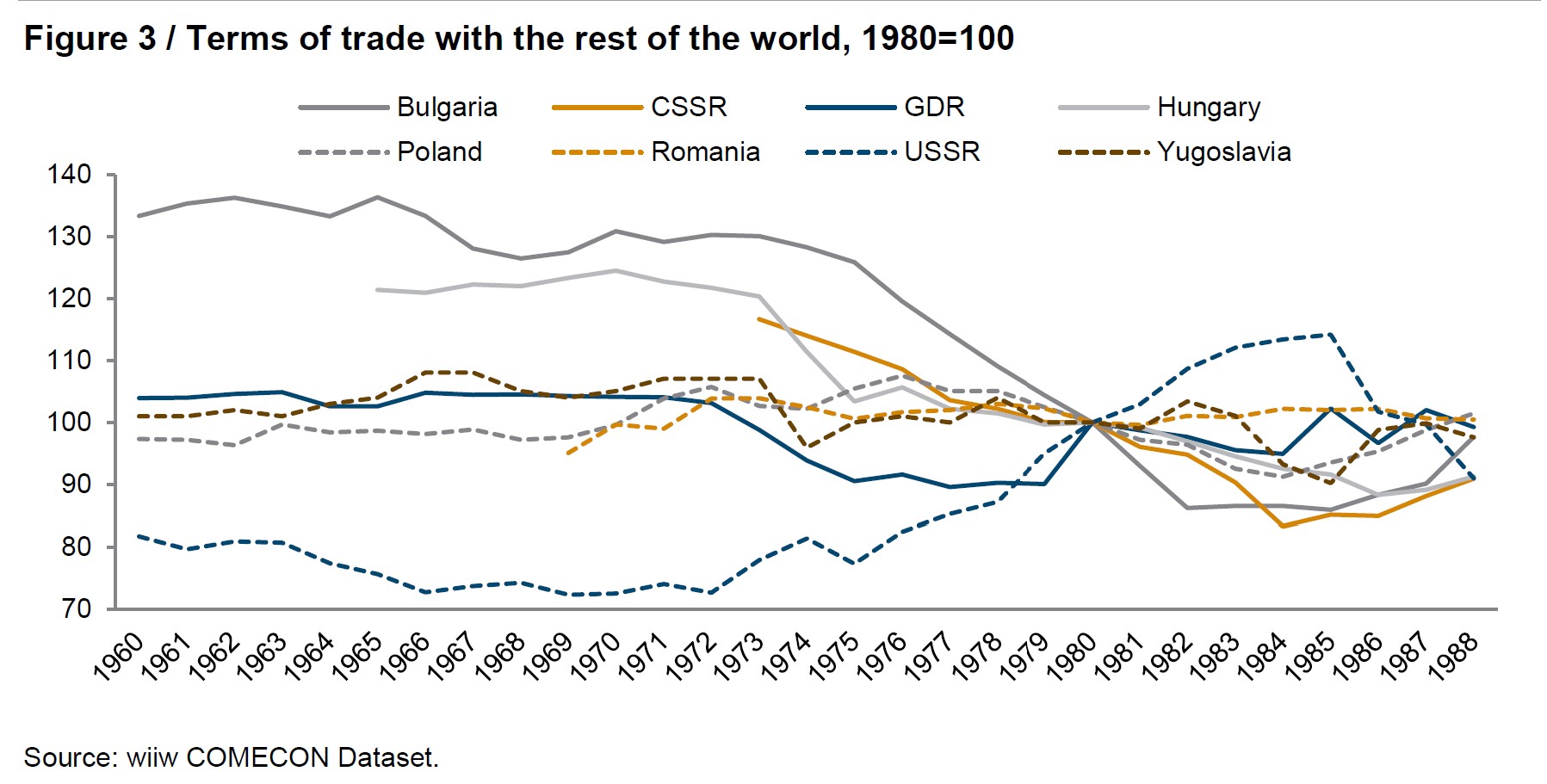

However, the impact of these shocks was not uniform (Figure 3). The Soviet Union benefited from improved terms of trade, while outcomes varied significantly across other COMECON countries. Romania and Yugoslavia fared relatively better, whereas Bulgaria and the CSSR struggled. In some cases, such as Bulgaria and the CSSR, the scale of the terms of trade shock may have overwhelmed any potential policy response. Yet, other countries experienced less severe impacts, suggesting that the collapse of socialism cannot be attributed solely to these external shocks.

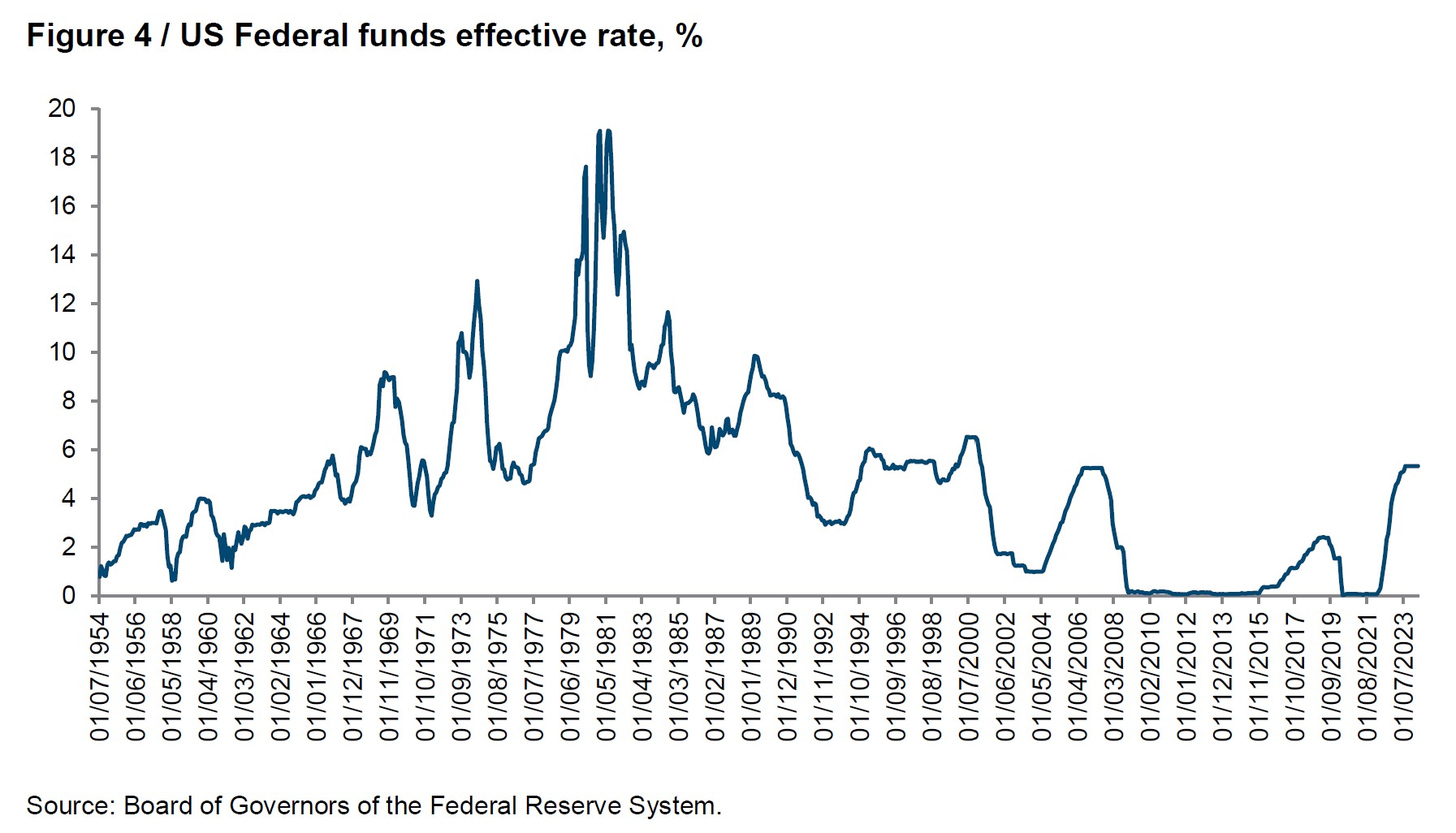

A related explanation is that due to the oil shocks and the corresponding inflation, the US Fed carried out the most significant monetary tightening in the post-war history, which had severe repercussions for the socialist countries. Indeed, the US Federal funds rate increased from around 5% in 1977 to 19% in 1981 (Figure 4). This led to a sharp rise in the debt service costs of the Eastern European countries.

According to Schmidt (1985) [3], in the 1970s socialist countries could borrow at annual interest rates of around 6%. By 1981, the interest rates they were paying had risen to 19% per annum. The situation was made even more challenging by the fact that these countries held primarily short-term debt, which required frequent refinancing. This left them highly vulnerable to sudden and sharp fluctuations in interest rates.

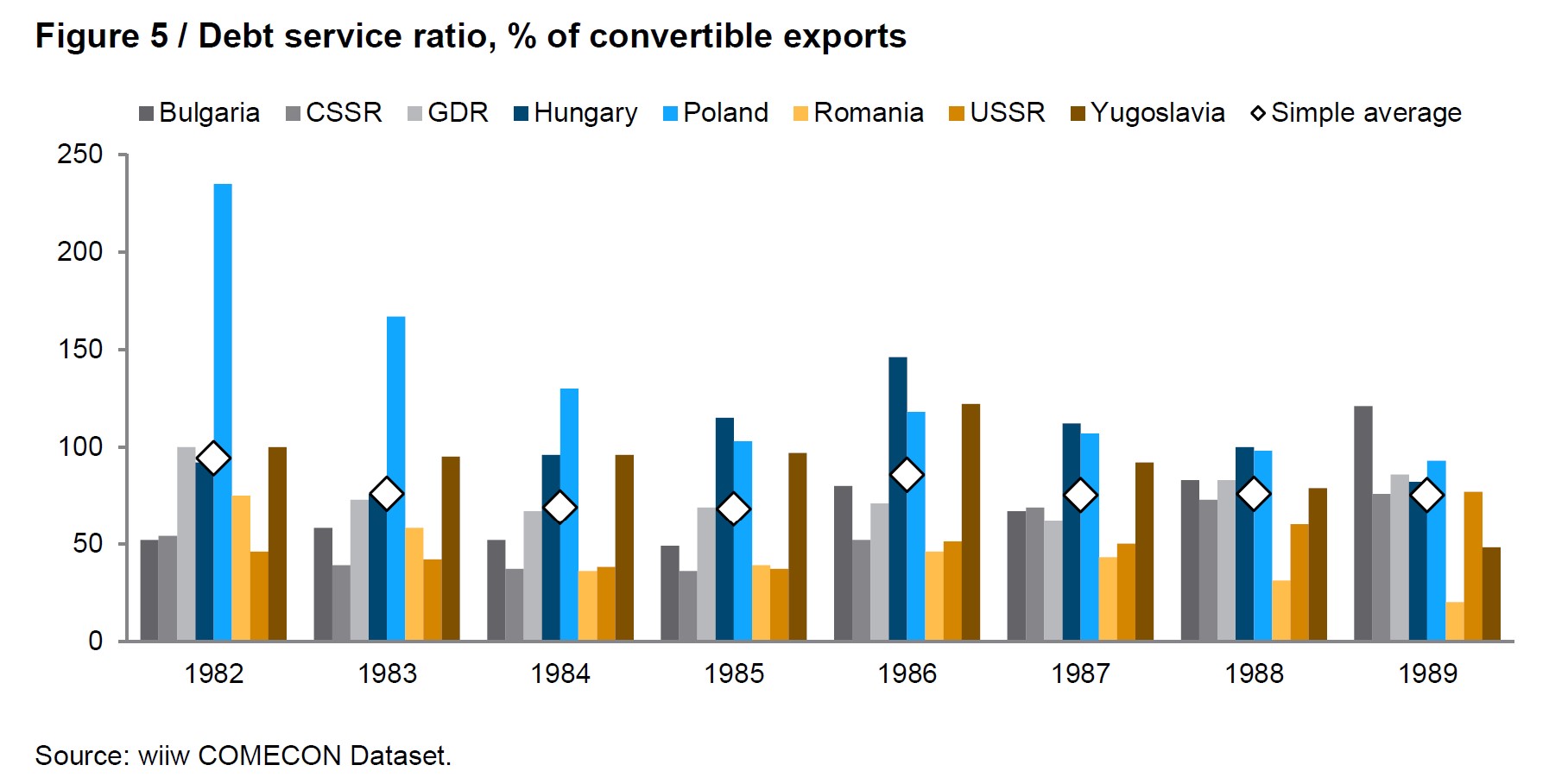

The high interest rates, combined with the relatively low convertible exports of the socialist countries (exports paid in hard currencies that could be used to repay debt), resulted in very high debt service ratios in the 1980s. This was especially the case in Poland, Hungary and Yugoslavia. In these three countries, annual debt service ratios during the 1980s were close to or even exceeded the value of all annual convertible exports (Figure 5).

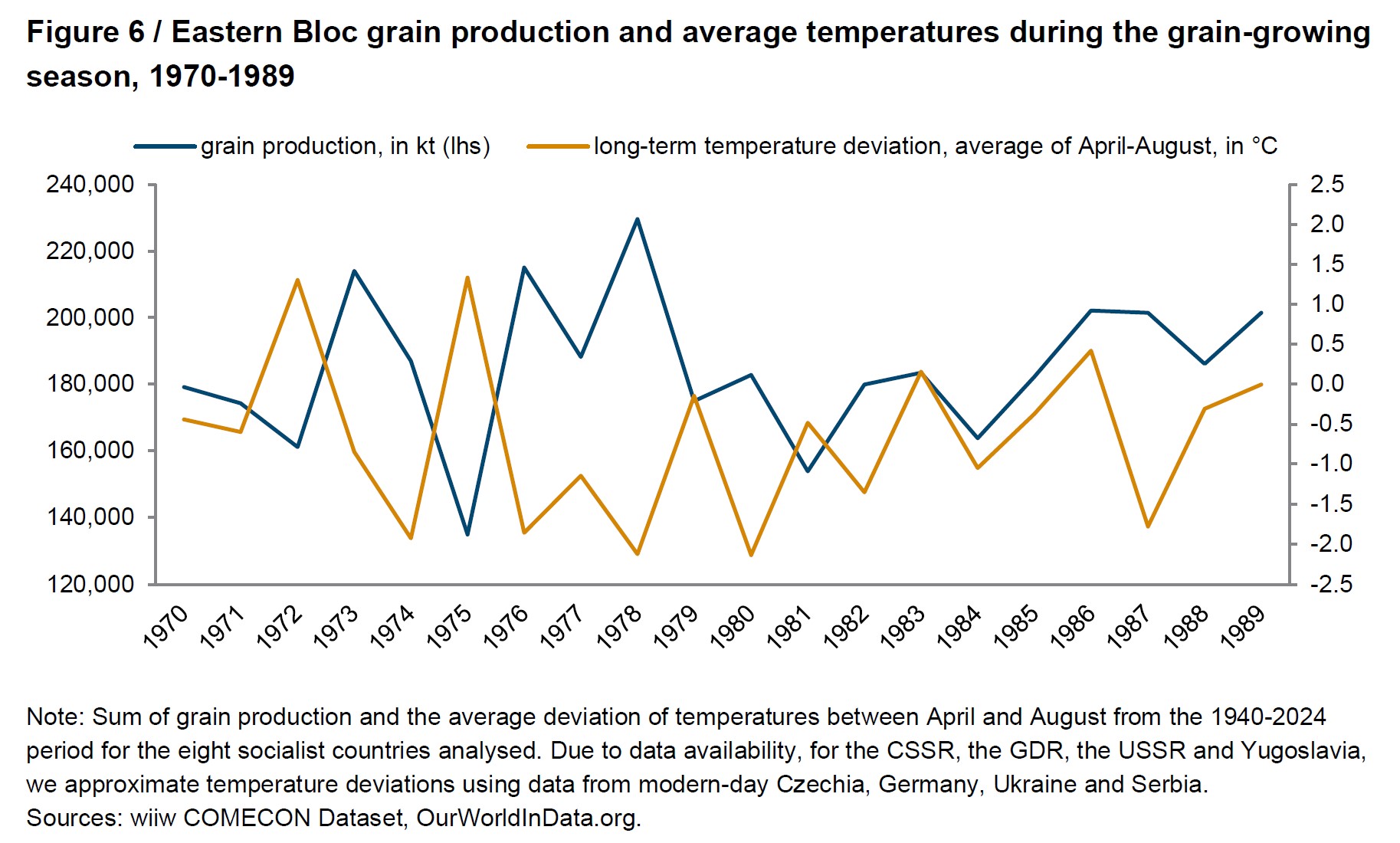

A final factor that we investigate in this group and that has not received a lot of attention in the literature, is related to the impact of weather and climate conditions on agriculture and economic activity. While average temperatures in the 1970s and 1980s were below the long-term average for the 1940-2024 period, individual years saw sharp temperature spikes. The years 1972 and 1975 were particularly severe, with spring and summer temperatures nearly 1.5°C above the long-term average. During years with higher temperatures in the grain-growing season (April to August), grain production in Eastern Europe declined sharply, with output dropping by 13% to 27% compared to the decade’s average (Figure 6).

Econometric analysis shown in the report shows that these above-average temperatures had a statistically significant negative impact on grain yields. Furthermore, a second econometric analysis established a strong positive relationship between grain production and economic growth, supporting the thesis that fluctuations in grain output significantly influenced national income growth. In other words, adverse weather conditions disrupted agriculture, a sector with an outsized role in Eastern European economies, and also had broader macroeconomic repercussions. Poor harvests not only strained trade balances but also hindered overall economic activity. Combined with the oil shocks and high interest rates of the same period, these climate-induced disruptions further constrained the capacity for growth in these economies.

The command system also had its flaws

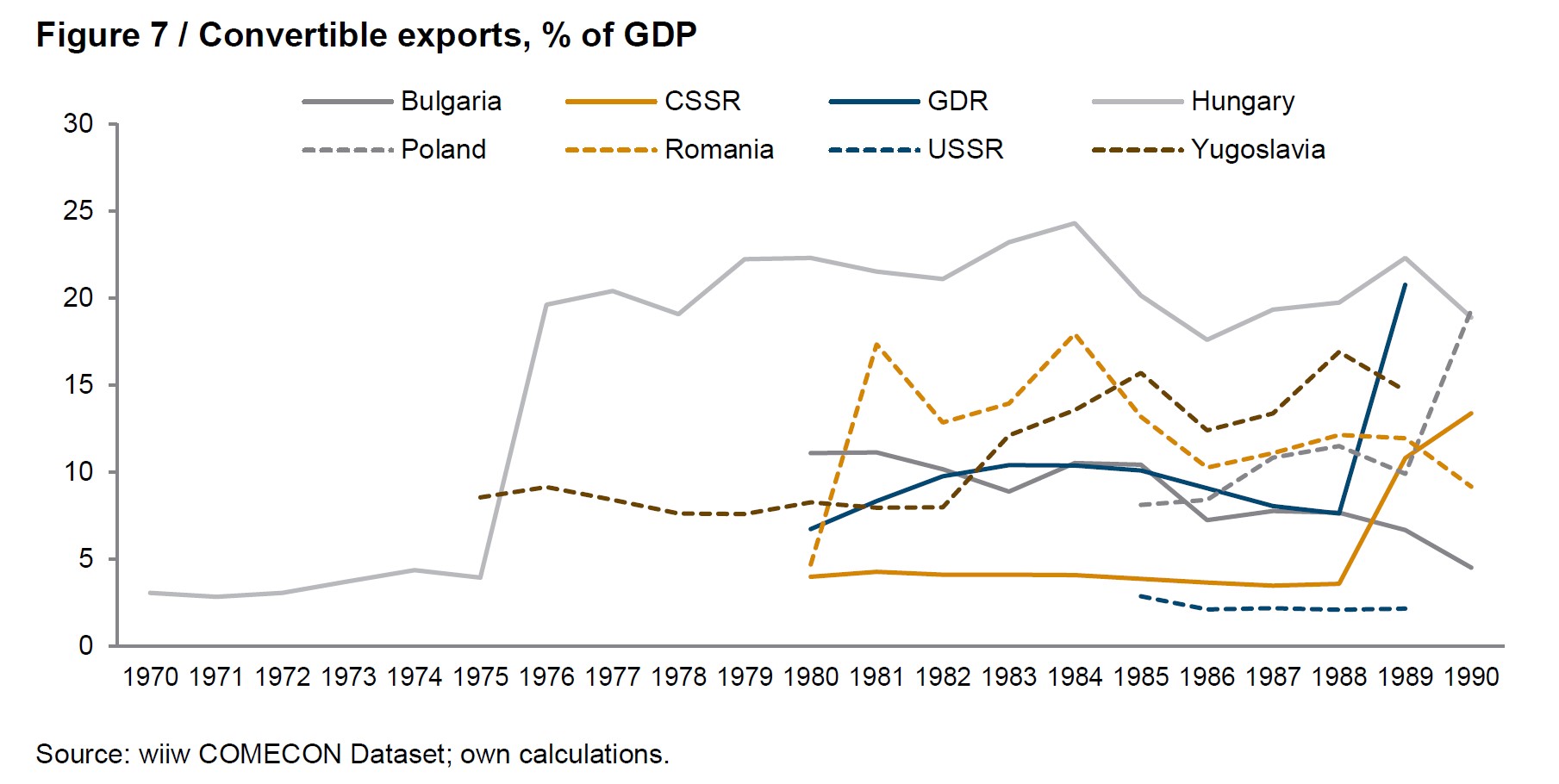

The primary reason the ex-socialist countries were hit hard by the rising interest rates of the late 1970s and early 1980s was their limited ability to generate convertible exports. During this period, only Hungary managed to achieve convertible exports exceeding 20% of GDP, while all other socialist countries remained below this threshold (Figure 7).

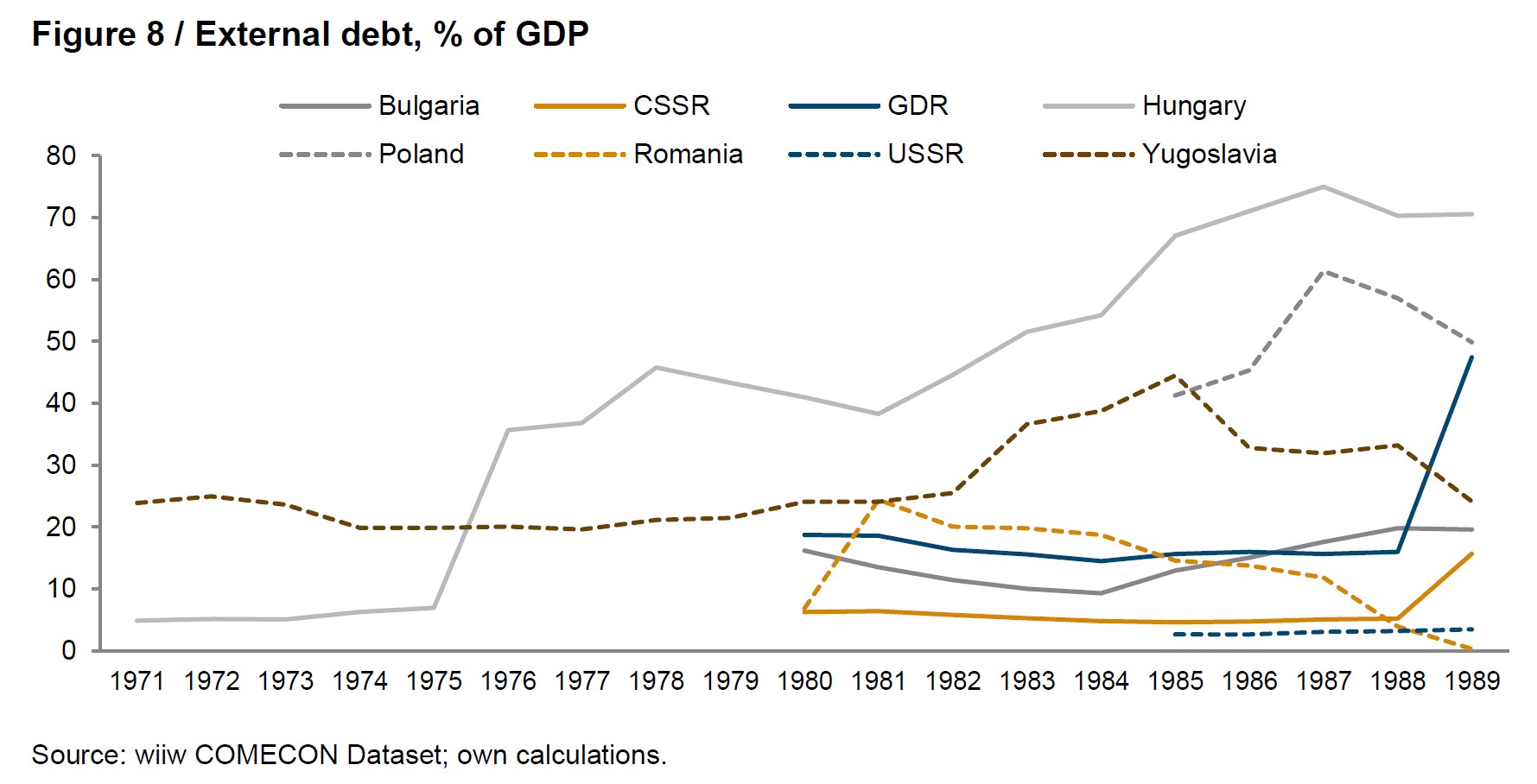

As a result of their low convertible export revenues, these countries struggled to service their external debt, even though their debt-to-GDP ratios were relatively low by contemporary standards. Hungary was the only country with relatively high external debt, reaching approximately 40% of GDP in the late 1970s and rising to 75% by the latter half of the 1980s. But even this would appear modest today. Poland’s external debt exceeded 60% by the mid-1980s, while Yugoslavia experienced an increase from 25% to 45% over the same period. Meanwhile, the other countries managed to keep their external debt levels around or below 20% of GDP throughout the 1980s (Figure 8). Despite these seemingly moderate debt ratios, the lack of sufficient hard currency revenues left these economies vulnerable to external shocks and limited their ability to navigate the rising global interest rates of the time.

The root cause of the problem lay in the countries' lack of competitiveness and technological backwardness, which led to the production of outdated, low-quality goods that struggled to compete in Western markets. Compounding this were political factors that reinforced their economic isolation.

Fearing that greater openness to the West might undermine socialism and pave the way for capitalism, these countries adopted restrictive trade policies and limited their integration with Western markets. This self-imposed isolation curtailed opportunities for economic modernisation and technological progress, leaving them further behind their Western counterparts.

Politicians made many mistakes as well

The first major policy mistake happened years before the problems became apparent. That was the insufficient investment in the first two decades after the Second World War. While the post-war growth was largely driven by a shift in labour from agriculture to more productive industry, investment rates in the East lagged behind those in the West throughout the 1950s and 1960s. This began to change in the 1970s and 1980s, but by then it was too late to reverse the trend. The underinvestment of the earlier decades likely contributed to the economic slowdown of the 1980s. However, it is important to acknowledge that weak investment in the immediate post-war years was not entirely a policy choice.

The demographic shocks of the war – such as widespread casualties, displacement and migration – led to labour shortages, which in turn constrained the capacity for investment.

The policies implemented in response to the oil shocks were also flawed. To secure hard currency for more expensive oil imports, many socialist countries redirected resources toward sectors with the greatest short-term export potential, such as low-productivity agriculture and food production, which had adverse long-term effects. At the same time, efforts to preserve hard currency led to restrictions on importing advanced Western technology, resulting in missed opportunities for productivity improvements and technological upgrading.

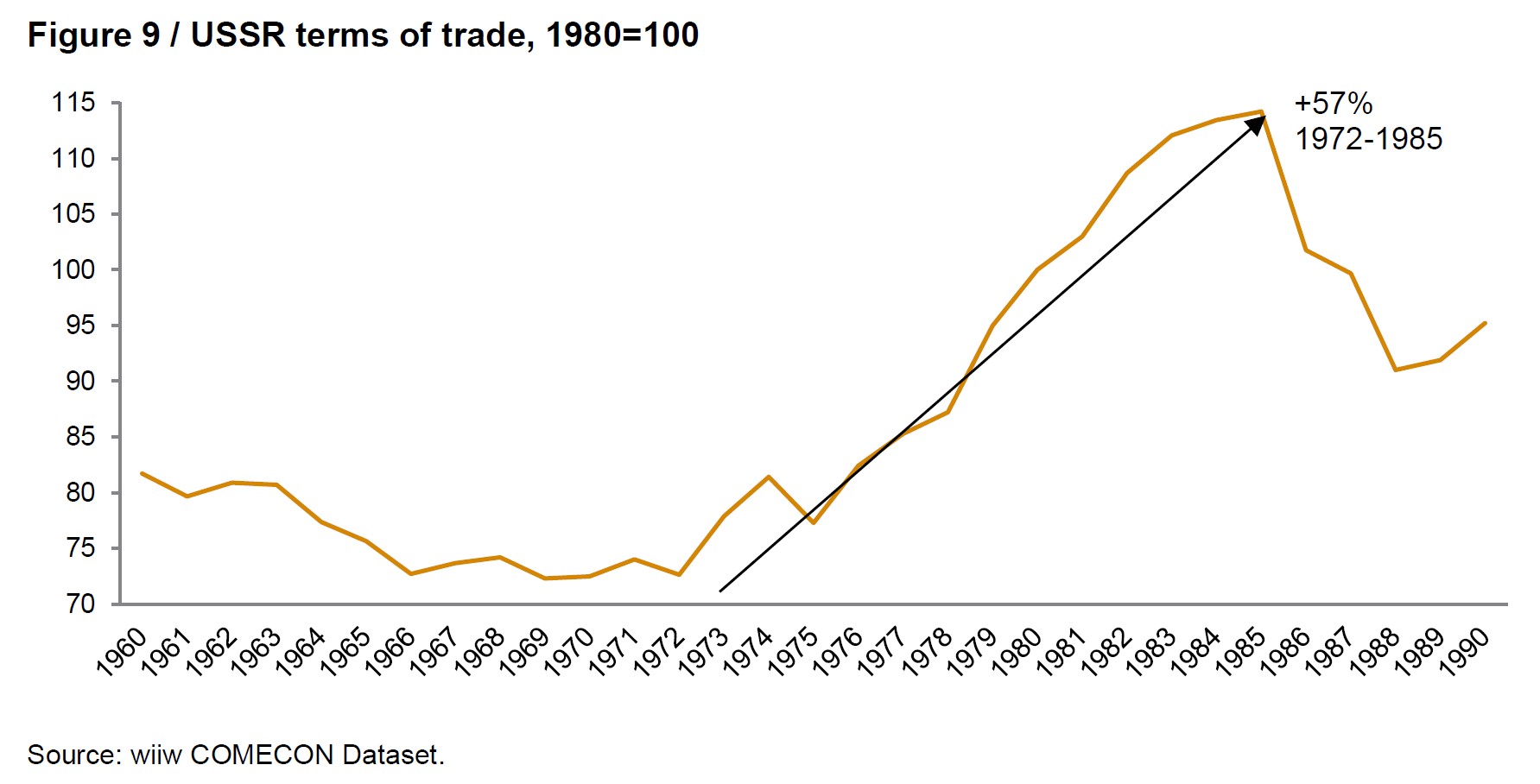

For the Soviet Union, the oil shocks initially provided a windfall. Between 1972 and 1985, the USSR experienced a significant and sustained improvement in its terms of trade (Figure 9). However, when oil prices collapsed sharply in the latter half of the 1980s, the USSR found itself dangerously exposed.

Compounding the problem, the Soviet Union, despite having the resources to continue subsidising other socialist countries, chose to start charging them market prices for oil in 1975, as explained before. It, in a way, abandoned its allies, which further deepened their economic struggles.

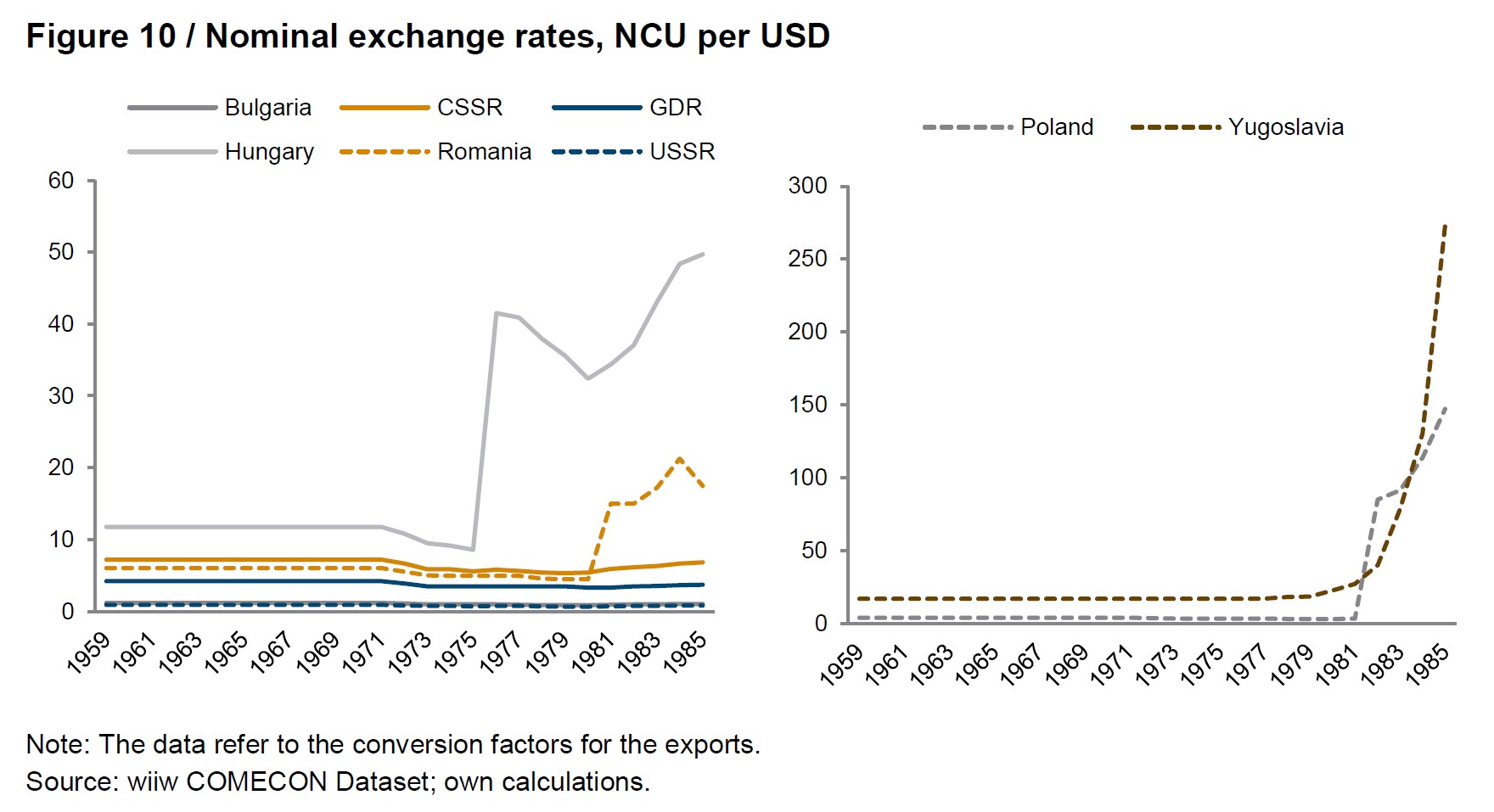

Another policy mistake was that many of the socialist countries devalued their currencies in the 1970s and 1980s, hoping to address current account problems but ultimately exacerbating them. In 1981, the Romanian leu was devalued threefold, from 4.5 ROL per USD in 1980 to 15 ROL per USD. Hungary saw its forint devalued fivefold in 1976, from 8.6 HUF per USD in 1975 to 41.5 HUF per USD. The Yugoslav dinar experienced an even steeper decline, devalued more than fifteenfold between 1979 and 1985, from 18.6 YUD per USD to 273 YUD per USD. Poland's zloty suffered the sharpest drop, devalued more than twentyfold in 1982, from 3.4 PLZ per USD in 1981 to 85 PLZ per USD (Figure 10).

The rationale behind these devaluations was the hope of reducing current account deficits by stimulating exports and curbing imports. However, this strategy was fundamentally flawed in the context of socialist economies, where the barriers to exporting to Western markets were structural rather than price-related.

Eastern Bloc products were already priced low, but their exports were constrained by poor quality, outdated technology, limited export capacity due to central planning, trade barriers and a lack of business knowledge and networks. In essence, both exports and imports were largely insensitive to price changes.

The trade regressions presented in our report support this conclusion. These regressions related convertible exports and imports to the nominal exchange rate (as a proxy for price competitiveness) and foreign/domestic GDP (as a proxy for income). The findings revealed that the exchange rate coefficient was statistically insignificant, while the GDP coefficient was highly significant and substantial in size.

This underscores that convertible trade flows in socialist countries were not influenced by exchange rate movements, making devaluations ineffective in addressing trade imbalances.

Rather than improving current account positions, these devaluations exacerbated inflation. A separate regression analysis showed that price levels in Eastern European countries between 1960 and 1990 were strongly and significantly affected by the nominal exchange rate. This suggests that the devaluations implemented during the 1970s and 1980s likely contributed to the inflation spikes that followed.

The resulting inflation reduced real incomes by driving up prices, which dampened consumption and economic activity. Moreover, devaluations raised debt servicing costs, as foreign loans became more expensive in domestic currency terms, further straining the already fragile financial systems of these economies. Instead of solving the problems they were meant to address, devaluations deepened economic instability.

A toxic mix that finished the patient

Thus, one could argue that the collapse of the socialist system resulted from a toxic mix of an unfavourable global environment, structural flaws within the command system and policy blunders by socialist policymakers.

Regarding the global environment, the oil shocks of the 1970s had a profound effect, especially for oil- importing socialist economies. Later, the oil price decline of the 1980s negatively impacted the Soviet Union. The Volcker interest rate shocks in the early 1980s further compounded these pressures, driving up debt servicing costs for countries that had borrowed heavily previously.

One underexplored factor we have found to be very important are the extreme weather events. High temperatures in 1972 and 1975 led to significant declines in grain production, reducing hard currency export revenues, worsening current account deficits and undermining economic activity.

The impact of these adverse external shocks was exacerbated by the structural limitations of command economies, which had low convertible export capacity due to their closed nature, low competitiveness and technological backwardness.

Policy mistakes further magnified these challenges. Major underinvestment before 1970 left these economies technologically behind, while misguided trade and export strategies in response to the 1970s oil shocks failed to address structural weaknesses. The Soviet Union squandered its oil windfall from 1973 to 1985, and exchange rate mismanagement in countries like Hungary, Poland, Romania, and Yugoslavia created additional financial pressures.

A particularly damaging decision was the Soviet Union’s 1975 shift from the Bucharest Principle of fixed five-year oil prices to the Moscow Principle of annually adjusted five-year moving averages tied to world market prices. This exposed other COMECON countries to the full force of the 1970s energy crisis, exacerbating their economic woes.

In the end, socialism collapsed because external shocks exposed and intensified the deep vulnerabilities of the socialist economies, which had been fragile and in need of reforms for some time. When these shocks struck, policymakers made decisions that not only failed to mitigate the damage but instead exacerbated the crisis.

Had any one of these factors been different – if external shocks had been less severe, if reforms had been implemented earlier, or if policymakers had made better decisions – it is possible that socialism might have endured. However, the interplay of these elements proved insurmountable, leaving us to think about these events and to write articles like this one.

wiiw’s COMECON database

As the article has shown, in the 1980s, just a few years before the collapse of communism in Eastern Europe, many Western analysts laboured under some severe misconceptions, leading them to vastly overestimate the economic power of the COMECON countries. This is hardly surprising: information on the economic composition of the Eastern Bloc was scarce, heavily biased and insufficiently detailed. In the COMECON countries themselves, the statistics were often manipulated for political reasons to conceal the communist system’s weaknesses.

To bridge this knowledge gap, the Vienna Institute of Economic Studies (wiiw) was established as an economic research institute specialising in those economies. From 1973 onward, the institute set out to map the economic realities of the COMECON countries. In this environment, its assessments became renowned throughout the world as one of the few sources of expert analysis and reliable data on the region.

Access the COMECON database here.

Footnotes

[1] Council for Mutual Economic Assistance, an economic organisation that existed from 1949 to 1991 under the leadership of the Soviet Union and that comprised the countries of the Eastern Bloc.

[2] Grieveson, R., Holzner, M., & Jovanović, B. (2024). The jockey, horse and racetrack revisited: Why did CESEE’s command economies collapse? (wiiw Research Report No. 477). Vienna Institute for International Economic Studies (wiiw). https://wiiw.ac.at/the-jockey-horse-and-racetrack-revisited-why-did-cesee-s-command-economies-collapse-dlp- 7080.pdf

[3] Schmidt, Paul-Günther (1985). Hard currency indebtedness of the developed socialist countries. Intereconomics, 20(3), 114–121. https://doi.org/10.1007/BF02928465