How compatible is economic convergence in the EU with its climate goals?

20 December 2022

The catching-up process in many regions is partly at odds with the goal of reducing greenhouse gas emissions to similar levels in all parts of the EU

image credit: wiiw

- Economic convergence is a topic widely discussed in the EU cohesion policy debate.

- Environmental convergence, on the other hand, is a new concept, born out of the substantial variations in greenhouse gas emissions across regions and the EU’s aim of becoming climate neutral by 2050.

- Economic convergence is not necessarily compatible with environmental convergence. The catching-up process in many regions of the EU is partly at odds with the goal of reducing greenhouse gas emissions to similar levels in all parts of the Union.

This article addresses the current state of, and expectations for, the economic and environmental convergence of the EU regions (at the NUTS-2 level). Regional economic convergence is not a new topic. It has been analysed since the late 1980s and early 1990s, starting with the seminal works of Barro and Sala-i-Martin (1992) and Sala-i-Martin (1996) and reaching its preliminary conclusions with the EU Commission's Eighth Report on Economic, Social and Territorial Cohesion (EU Commission, 2022).

Economic convergence has slowed markedly

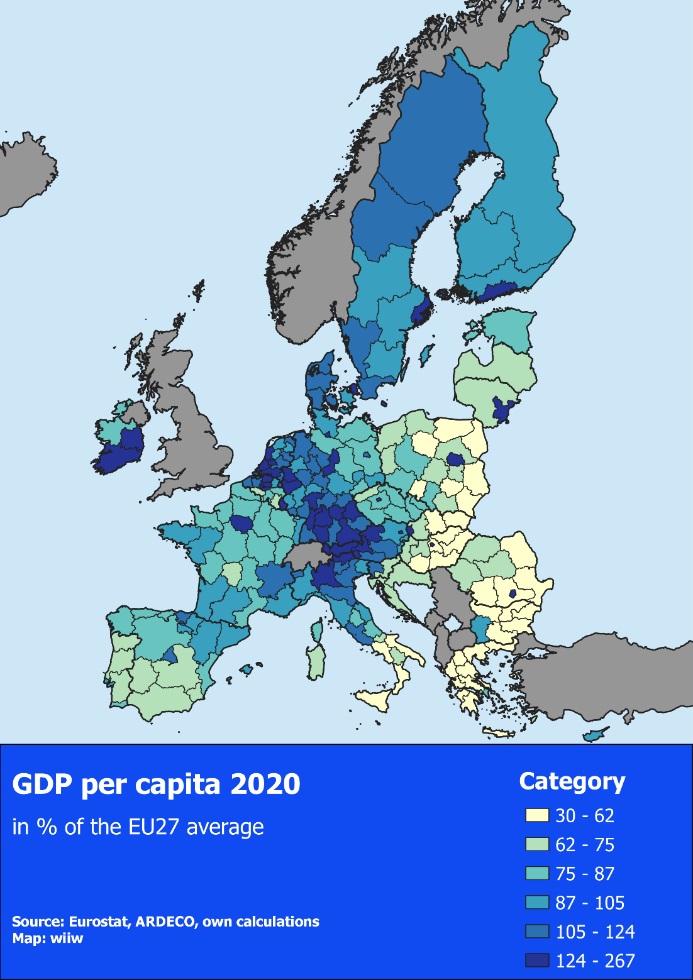

Regarding the current state of economic convergence of the EU NUTS-2 regions, the main assessment is that regional economic disparities are still substantial. This is illustrated in Figure 1, which shows regional GDP per capita in purchasing power standards (PPS) in 2020.

Figure 1 - Regional GDP per capita in PPS in 2020, as a percentage of the EU average

Source: Eurostat ARDECO database, own calculations.

It shows that those regions with the lowest GDP per capita (i.e. as low as one third of the EU27 average) are located in Central and Eastern Europe (EU-CEE), and include eastern regions of Poland, Slovakia and Hungary, as well as some regions of Romania and Bulgaria, and large parts of Greece. Regions in Southern Italy, Spain and Portugal (except Lisbon), the western parts of Poland, Slovakia and Hungary, as well as most regions of Czechia, record slightly higher levels of GDP per capita, although they are still at the lower end of the EU regions, reaching at best 75% of the EU average. Many regions of France and Eastern Germany have levels around the EU27 average, while the highest levels are recorded in Northern Italy, Austria, Western Germany, the Benelux countries, Scandinavia and Ireland. Notably, most of the capital cities of Europe, regardless of country, are among the regions with the highest GDP per capita in PPS terms.

Over the past decade, Europe has experienced a phase during which the EU-CEE regions have caught up rapidly. The major driver behind this has been the structural change in the EU-CEE economies from low value-added to higher value-added activities. The Eighth Cohesion Report (EU Commission, 2022) finds that the strong growth observed in EU-CEE has also been due to high returns on infrastructure investment and low-cost advantages. However, these advantages are now beginning to disappear, slowing the convergence process of the EU-CEE regions.

Many Southern EU regions, particularly in Greece, but also Southern Italy, Spain and Portugal, arguably face even greater challenges. They have never fully recovered from the 2008/2009 economic and financial crisis, and have recorded low to very low economic growth over the past decade. The Eighth Cohesion Report suggests that those regions have entered the so-called ‘development trap’, where they find it hard to compete both with regions with a lower level of GDP per capita (in terms of labour costs) and with regions with a higher level of GDP per capita (in terms of economic structure).

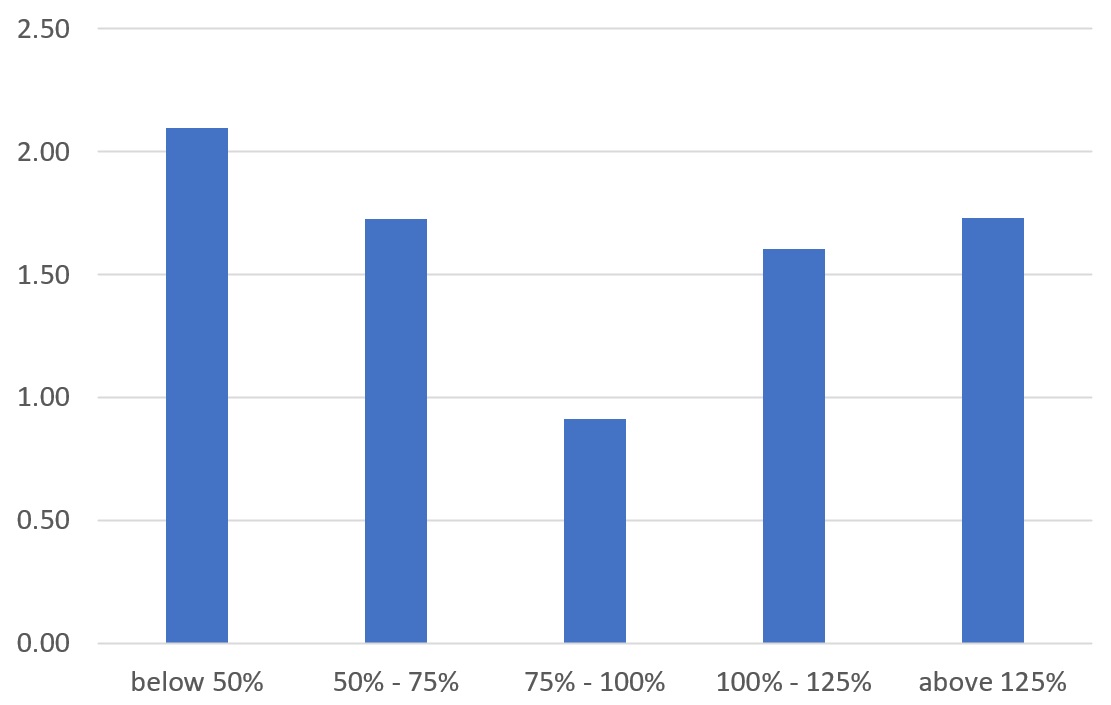

These developments are reflected in the real GDP per capita growth of EU regions, shown in Figure 2. This demonstrates that overall, the regional economic convergence process has witnessed a slowdown in recent years. On average, the poorest regions – i.e. those with GDP per capita levels below 50% of the EU27 average – had the highest growth in 2009-2019, at around 2.1% per year. However, the second-highest growth rate (1.7% per year on average) was recorded by the richest regions. On average, the lowest growth rate (only 0.9% on average) was recorded in those regions with GDP per capita levels of between 75% and 100% of the EU average.

Figure 2 - Real GDP per capita growth in EU regions, annual averages over 2009-2019, in %

Notes: simple averages; regions are grouped according to GDP per capita as a percentage of the EU27 average in 2009.

Source: ARDECO database, own calculations.

The Eighth Cohesion Report of the European Commission suggests that, in order for the less-developed EU-CEE regions to maintain high economic growth and for Southern EU regions to escape from the ‘development trap’, they need to implement strong public sector reforms, upgrade skills and improve their innovative potential.

Is economic convergence compatible with environmental convergence?

Unlike economic convergence, environmental convergence is not a commonly used expression. Yet, to our mind, it is an appropriate one, given the substantial variations in greenhouse gas (GHG) emissions at the national and regional level in the EU, as well as the EU’s goal of ‘increas[ing] the greenhouse gas emissions reduction target for 2030 to 55%’ (compared to the 1990 level), with the aim of transforming the EU into a climate-neutral economy by 2050 (EU Commission, 2020a and 2020b). This implies that, as of 2022, certain EU member states and regions are relatively close to fulfilling those EU targets, whereas for others there is still a long way to go. Since in the end, all EU countries and regions need to become climate neutral by 2050, the regions with high GHG emissions need to reduce their emissions by more than other regions. In a sense, this corresponds to an environmental convergence process.

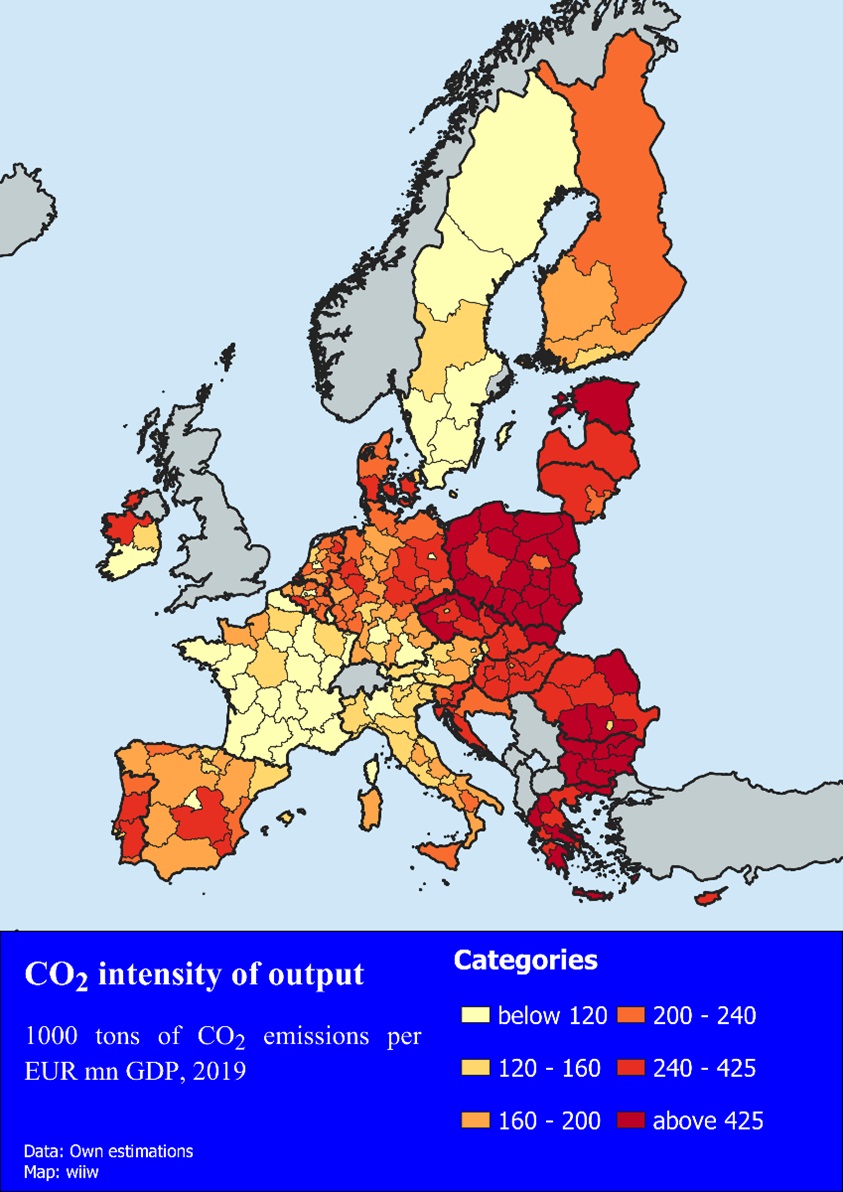

To analyse empirically the need of the EU NUTS-2 regions to converge environmentally, we estimate their CO2 intensity, i.e. their CO2 emissions per unit of GDP. For this, we use Eurostat statistics on country-level GHG emissions by detailed industry groups (at the NACE rev.2 two-digit level) and match them with equally detailed employment data at the regional level. This results in an estimate for regional CO2 emissions by individual industry. These data are then aggregated to give total CO2 emissions (in tonnes) for each EU NUTS-2 region. As a final step, we calculate the ratio of CO2 emissions to regional GDP, in order to arrive at regional CO2 intensity.

The result of this estimation is illustrated in Figure 3. It indicates very high disparities in CO2 intensities across the European regions. They are lowest in France and Sweden, followed by Northern Italy, Austria and Southern Germany. By contrast, CO2 intensities are high throughout EU-CEE, as well as in Greece, with levels that are three times (or more) the levels in the regions with the lowest CO2 intensity.

Figure 3 - CO2 intensity of regional output, 2019 (thousand tonnes of CO2 emissions per EUR mn of GDP)

Source: Eurostat, own estimations.

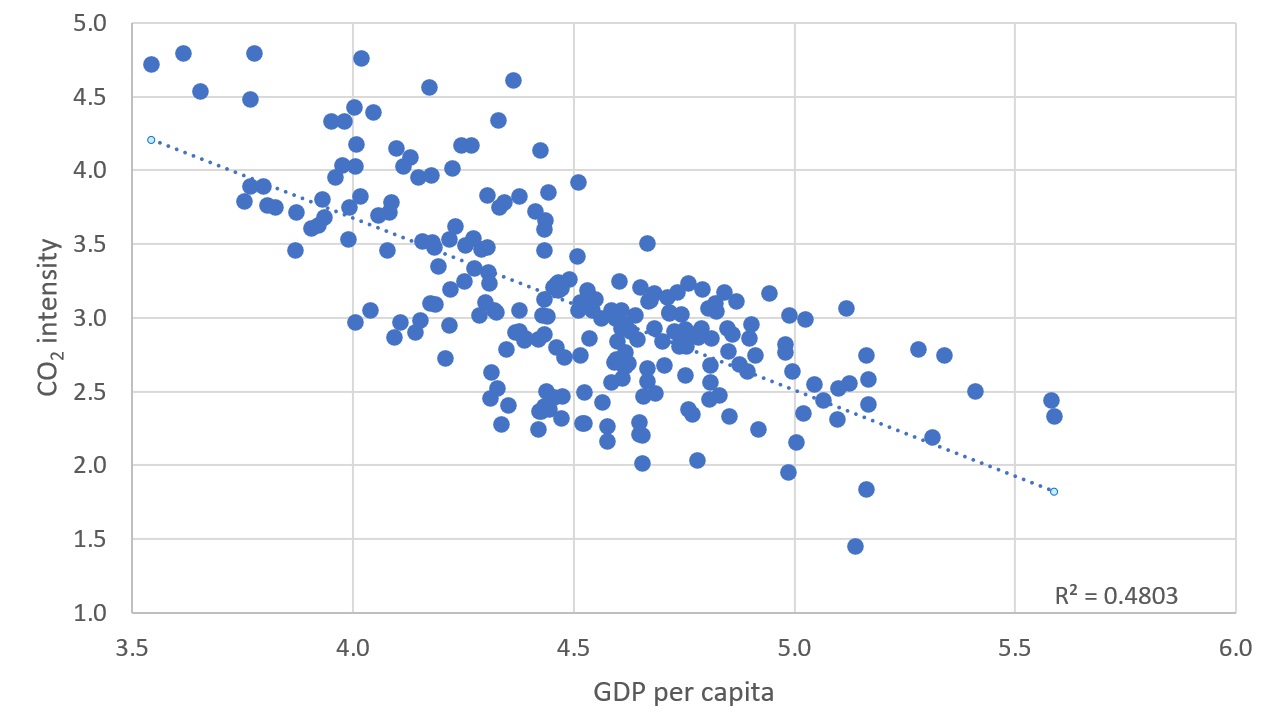

Matching CO2 intensity with GDP per capita data at the regional level (see Figure 4) indicates a strong relationship between economic and environmental convergence, as the poorest regions are, as a rule, also those with the highest CO2 intensities. Thus, those regions face a dual convergence challenge, requiring simultaneous economic and environmental convergence.

Figure 4 - Correlation of CO2 intensity and GDP per capita in PPS in EU regions, 2020

Note: values in logarithms.

Source: Eurostat, own estimation.

This may create a dilemma for low-income regions, as studies suggest that economic growth increases energy consumption and, all other things being equal, GHG emissions. Therefore, if we consider three of the main sectors that contribute to GHG emissions – transport, housing and manufacturing – reaching CO2 neutrality could be a particular challenge for the less-developed EU regions. For them, reducing GHG emissions in the transport sector and housing by switching from fossil fuel-powered cars to environmentally friendly forms of transport and by increasing the energy efficiency of housing is more burdensome than for other regions. As a rule, their transport and housing sectors are more energy intensive than those of more-developed regions. Thus, the replacement/renovation requirements are disproportionately great. Second, their capacity to invest in GHG-reducing technologies is lower than in other regions. As a consequence, they may need to invest a higher share of their GDP in CO2 neutrality, in order to reach goals similar to those of the more-developed regions.

Additionally, CO2 neutrality is a particular challenge for EU regions that specialise in carbon-intensive industries, such as fossil fuel production, the steel industry, basic chemicals (ethylene and ammonia) or cement production. Those sectors are very energy intensive, and therefore will undergo the most dramatic technological changes – either through increased use of alternative energy sources or through new production technologies that reduce fossil energy demand and, as a consequence, GHG emissions. The problem for economic growth is that these changes require investment in new, GHG-reducing capital stock, without necessarily raising the level of potential output. Thus, these industries will incur significant sunk costs, which – if the environmental investments crowd out other investments – will have little positive effect on economic growth.

Simultaneously, the economic benefits of achieving CO2 neutrality are likely to be reaped by the more competitive and innovative European regions that have the ability to develop and produce the environmentally friendly technologies needed for the ecological transformation of the European economy. In most cases, these are the economically strong regions of Europe. Thus, while the less-developed regions will be disproportionately challenged by the green transition, the economically strong regions could benefit from it. If that is the case, the attempt to achieve CO2 neutrality by 2050 will have a negative impact on economic convergence and cohesion within the EU.

References