Larger-than-expected US tariff hikes will hit many countries hard

03 April 2025

An overview of the US tariff hikes announced on 2 April and an assessment of their impact: The consequences will be significant for countries with strong ties to the US as well as for those facing steep tariff increases

image credit: unsplash.com

By Oliver Reiter and Robert Stehrer

The tariff scheme announced by the Trump administration is worse than expected. The main reason is that the assessment considered not only monetary tariffs but also non-monetary barriers, such as undervalued currencies and other related claims, all of which are summarised in a detailed report. The 400-page report dedicates 29 pages to the EU, highlighting, in addition to tariffs, issues like import licensing for bananas, technical barriers to trade (TBT), sanitary and phytosanitary (SPS) measures related to European standards, procurement rules, intellectual property rights (IPRs) and service barriers. Similar assessments are carried out for many other countries.

All of this seems rather complicated on first glance. But, in fact, the calculations of the tariff rates have been much simpler. As is stated on the website of the Office of the United States Trade Representative[1]: ‘Reciprocal tariffs are calculated as the tariff rate necessary to balance bilateral trade deficits between the U.S. and each of our trading partners. This calculation assumes that persistent trade deficits are due to a combination of tariff and non-tariff factors that prevent trade from balancing. Tariffs work through direct reductions of imports.’

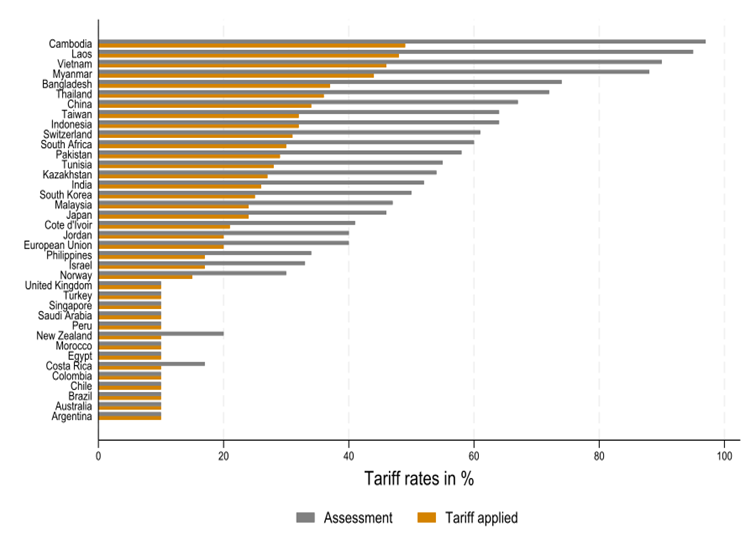

Based on these considerations, huge ‘reciprocal tariffs’ have been calculated – but the actual rates to be applied will only be roughly half of the calculated rates (As Trump noted: ‘This is not full reciprocal, it is kind reciprocal.’) (see Figure 1). For example, this means a tariff increase of 34% for China (down from the assessed 67%, although the actual rate including earlier tariffs will be 54%), 20% for the EU (from 39%), 46% for Vietnam (from 90%), 32% for Taiwan (from 64%), 24% for Japan (from 46%), 26% for India (from 52%), 30% for South Africa (from 60%), and so on. In general, a ‘baseline’ tariff rate of 10% has been announced for all countries (e.g. the UK and Brazil) and products. It is interesting to note that traditional US allies, such as South Korea (25%), Japan (24%), and Taiwan (32%), will face very high tariffs. Second, it is noteworthy that Russia does not appear on the list at all.

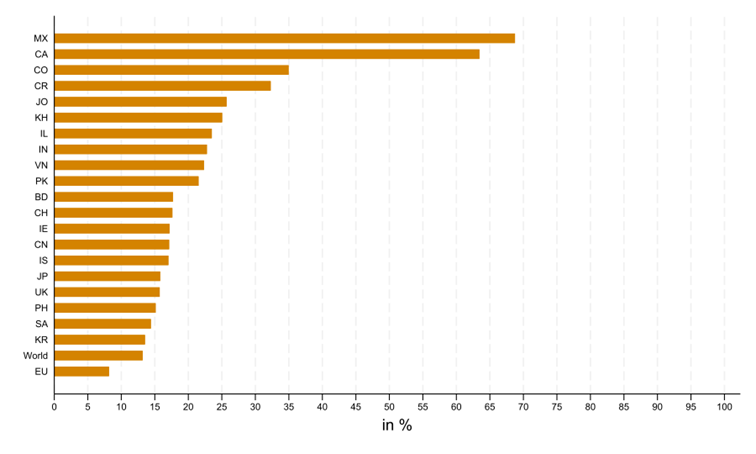

The tariff hikes primarily impact countries facing significant increases in tariffs (see Figure 1) and those with strong trade linkages to the US, such as Colombia, Costa Rica, Cambodia, Israel and India (see Figure 2). In the EU, approximately 7% of gross exports go to the US.

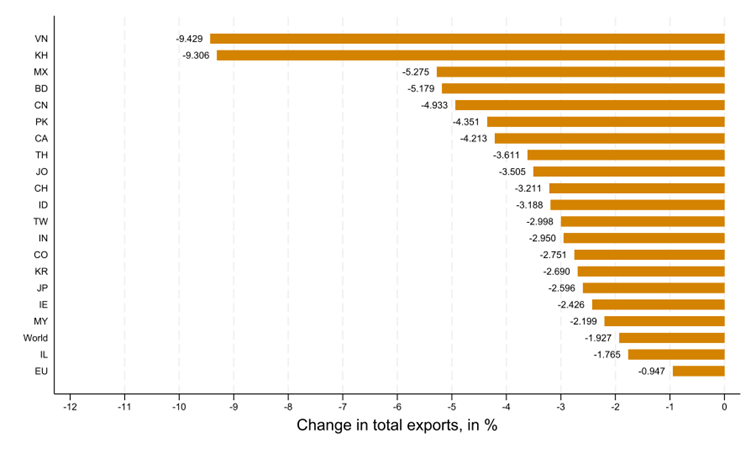

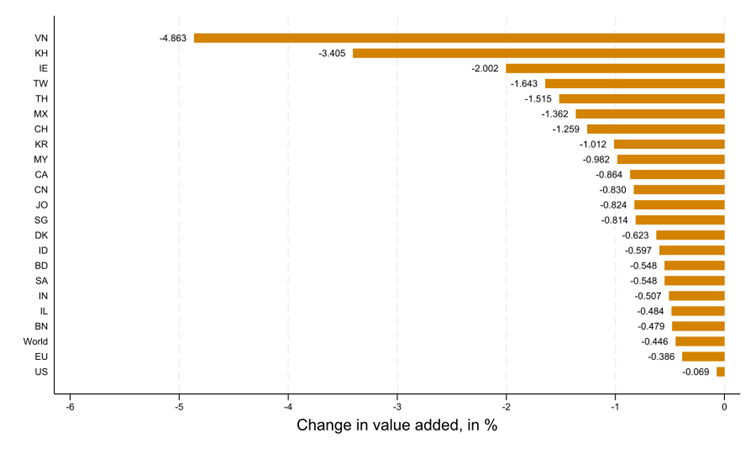

In a preliminary assessment, we model the impacts of these tariff hikes within an input-output framework, assuming a decline in exports corresponding to the increase in the tariff rate. The results are presented in Figure 3 for exports and total value added. Vietnam and Cambodia will see a decline in their overall exports of nearly 10%, while Bangladesh, China, Pakistan and China (again) will experience declines ranging between 4% and 5%. Total EU exports would decrease by 1%.

Figure 1 / Announced tariff rates

Source: Own assessment.

Figure 2 / Share of gross exports to US in total gross exports, 2020

Figure 3 / Short-term effects of the tariff hikes

Exports

Value added

Source: OECD TiVA, own calculations.

This decline in exports could have severe negative impacts on the respective country’s GDP, which – according to these calculations – would decrease by almost 5% for Vietnam, by 3% for Cambodia, by 2% for Ireland, and by more than 1% for China, Mexico, Thailand and Taiwan. The EU’s GDP would decline by about 0.4%, with similar effects for Austria and Germany, according to these preliminary calculations.

Footnote:

1] See also https://x.com/Geiger_Capital/status/1907568233239949431?s=09.