'Output gap nonsense': Understanding the budget conflict between the EC and Italy’s government

17 June 2019

The European Commission’s assessment of the state of the Italian economy lacks macroeconomic plausibility. Fiscal policy recommendations need to change.

By Philipp Heimberger

Photo: iStock.com/Silvia Cozzi

- The European Commission’s recommendation for starting an excessive deficit procedure against Italy is based on the controversial technocratic assessment that Italy’s economy is not really in deep crisis.

- This assessment builds on the Commission’s model-estimations of the so-called 'output gap', which is estimated to be very low.

- Low output gap estimates lack macroeconomic plausibility: slack is still substantial as unemployment remains above 10%, youth unemployment is above 30% and headline inflation is too low at 1%.

- The Commission’s recommendations on Italian fiscal policy would need to be different if the degree of underutilization of economic resources in the Italian economy was estimated to be higher.

The conflict about Italy’s public budget has entered a new phase. On June 5th, the European Commission recommended the opening of an excessive deficit procedure because of violations of the EU’s rules on public debt. The European Commission vehemently opposes the Italian government’s plans for cuts in taxes and increases in government spending. Now, the EU’s finance ministers will have to decide on the Commission’s recommendation regarding a new excessive deficit procedure for Italy.

For the year 2019, the European Commission expects – based on its latest macroeconomic forecast – that the Italian budget deficit will be 2.5% of GDP. This would already be higher than the Commission is willing to accept within Italy’s medium-term budgetary path. For the year 2020, Italy’s budget deficit is currently forecast to widen to 3.5% of GDP – which would be above the 3% deficit limit in the EU’s fiscal rules. Against the background of very low economic growth rates over recent years, Italy’s public-debt is expected to remain persistently high at more than 130% of GDP.

Media coverage of the Italian budget has strongly focused on high public debt. However, one aspect has received little attention, although it is highly relevant: The dismissive position of the European Commission regarding the Italian government’s fiscal plans is firmly based on a technocratic assessment of the state of the Italian economy. Economists working at the Commission use a macroeconomic model to estimate that Italy’s economy currently does not suffer from underutilization of economic resources, and, hence, is not really in crisis: for the years 2019 and 2020, the so-called “output gap” is estimated to stand at -0.3% and -0.1% of GDP, respectively. This assessment implies that there is no space for expansionary economic policies to stimulate growth, because such measures would run the risk of an 'overheating' labor market and accelerating inflation. In its recently published recommendations for Italy, the European Commission explicitly refers to this controversial assessment on the output gap.

What is the state of the Italian economy?

The output gap is an economic concept, which – in theory – indicates the cyclical position of an economy. If actual output (measured in terms of GDP) is above potential output, the output gap is positive, and the economy is “over-heated”. If actual output is below potential output, the output gap is negative, which indicates an underutilization of economic resources. In this context, potential output is defined as the (unobservable) level of output in an economy at which all production factors are employed at non-inflationary levels.

Currently, the European Commission estimates Italy’s output gap for the years 2019 and 2020 to stand at -0.3% and -0.1% of GDP, respectively. In other words: the Commission thinks that the Italian government is only producing marginally less than it could potentially produce if the production factors labor and capital were utilized “normally”, i.e. at non-inflationary levels.

Based on this logic, the European Commission sees no room for fiscal maneuvering, as expansionary policies would only risk an 'overheating' Italian labor market and accelerating inflation. Only higher negative output gaps (e.g. of -2% of GDP or more) would indicate substantial slack in the Italian economy, so that expansionary policy measures (such as higher public investment) could help to close the output gap.

Nonsense output gaps

The European Commission’s estimates of the output gap are startling if one considers that the unemployment rate in Italy in the year 2019 is expected to remain high at 10.9%, while the Italian economy is in quasi-permanent crisis, which has also lead to worryingly low inflation rates. Youth unemployment currently stands at more than 30%.

Because of such controversial model-based assessments, Robin Brooks and Adam Tooze have recently launched a campaign against 'nonsense output gaps'. Their criticism is based on an argument that the underlying estimates of the output gap for countries such as Italy are implausible from an economic point of view, because it is likely that existing slack is much higher than suggested by the Commission’s official estimates, and existing estimation problems promote excessively restrictive policies.

As the output gap critique put forward by Brooks and Tooze directly refers to two studies, which I have co-authored with Jakob Kapeller and Jakob Huber, it will not come as a surprise that I share their criticism. However, given the new round of escalation regarding the Italian budget it seems necessary to explain the underlying problems in more detail and to illustrate them based on a case study. This seemingly technical question is also highly important for the future stance of fiscal policy in other euro area countries.

The relevance of the output gap in the EU’s fiscal regulation framework

The conflict between the Italian government and the European Commission about Italy’s budgetary plans already started in summer 2018, but it has now entered the next phase. In this standoff, the importance of output gap calculations has been largely hidden from the public debate, although the output gap represents the technical core of the EU’s fiscal rules. Estimates of the output gap shape the room for fiscal maneuvering of EU member countries: medium-term budgetary objectives relate to the ‘structural’ deficit, which directly depends on the size of the output gap.

In theory, the ‘structural’ deficit is the part of the headline budget deficit that actually affects long-term debt sustainability, because it is not due to cyclical fluctuations. At the core of the EU’s fiscal rules, the yearly ‘structural’ deficit limit is limited at 0.5% of GDP (with several exceptions and additional requirements). But in the form of so-called “debt brakes”, medium-term ‘structural’ deficit targets were also put into national law, e.g. in Germany, Italy, Austria and Spain.

In case of a violation of budgetary targets based on the ‘structural’ deficit, the respective government is required to implement fiscal consolidation measures (i.e. tax increases and/or expenditure cuts) to correct the ‘excessive’ deficit. The basic idea is that the ups and downs of the business cycle affect government revenues and expenditures, but these temporary effects should be subtracted from the headline budget balance to get a clearer perspective on the ‘structural’ fiscal situation. In its report on Italy, the European Commission explicitly requires the Italian government to implement fiscal consolidation measures, because recent budgetary plans are expected to violate the medium-term ‘structural’ budget targets.

If the output gap is estimated to be strongly negative (which would indicate substantial underutilization of economic resources), only a small part of the actual fiscal deficit is assessed to be ‘structural’ – implying that the respective government is not required to implement fiscal consolidation measures. If, however, the output gap is estimated to be rather small, a large part of the actual fiscal deficit is considered to be ‘structural’ and, hence, has to be addressed by fiscal consolidation efforts.

It is important to understand that the output gap is non-observable, as it has to be estimated based on an economic model. For doing so, the European Commission has developed its own model over the last 20 years. This model has been adjusted over time, and its estimates have been challenged by several EU member states pointing to their lack of macroeconomic plausibility.

Output gap scenarios for Italy

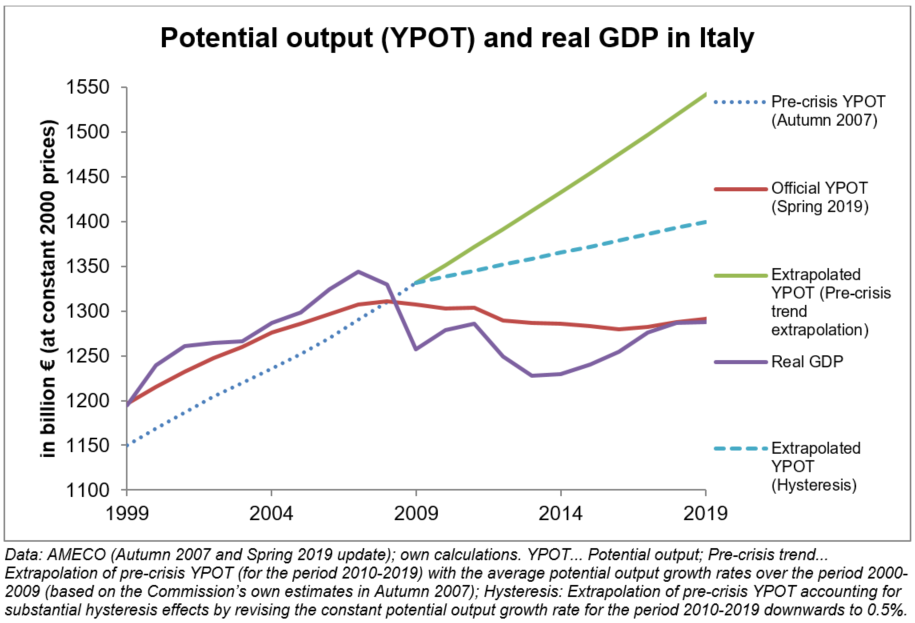

For the years 2019 and 2020, the European Commission estimates that the output gap of the Italian economy will stand at -0.3% and -0.1% of GDP, respectively. This assessment results from the difference between inflation-adjusted GDP (actual output) and the model-based estimates of potential output – the unobservable level of economic activity at which the Italian economy would be neither overheated nor underutilized. The figure below shows that actual output is only minimally below the Commission’s official potential output estimate.

The persistent crisis of the Italian economy over recent years had a strong impact on the Commission’s potential output estimates. To illustrate this point, we extrapolate the pre-crisis developments in potential output: in particular, we use the Commissions model-based potential output estimates produced back in 2007 (before the start of the financial and economic crisis), and extend them by using a constant growth trend for the years 2010-2019, where the extrapolation is based on the average potential output growth rates from the 2000-2009 period.

The results are striking: using this simple trend extrapolation, we find a large negative output gap (the difference between actual output and potential output) of -16.5% of GDP for the year 2019, which starkly contrasts with the official Commission estimate of -0.3%.

A simple trend extrapolation is arguably problematic, since the macroeconomic effects of the crisis may have led to an overestimation of potential output growth. Downward revisions may be justified insofar as the crisis has triggered 'hysteresis effects'. The concept of hysteresis postulates that inadequate demand during crisis times may have long-run effects on the supply-side potential of an economy, e.g. when long-term unemployment leads to skill losses among those who lost their jobs during the crisis.

To account for this hysteresis argument, we assume that the crisis has indeed drastically reduced the growth in potential output for the Italian economy. Over the period 2000-2009, the average growth rate of potential output was estimated to be 1.5% (based on the Commission estimates in autumn 2007). As can be seen from the figure above, the negative output gap remains substantial (-8.0% of GDP) if we allow for large hysteresis effects. Even in this alternative scenario, expansionary fiscal policies could certainly be used to stimulate the Italian economy without running the risk of an “overheating” of the Italian labor market and accelerating inflation.

Larger output gaps lead to ‘structural’ budget surpluses

We can demonstrate the relevance of current output gap estimations for Italy by looking at their implications for the room that can be used by the Italian government for fiscal policy maneuvering. The Commission currently estimates that the Italian budget deficit will come in at 2.5% of GDP in 2019, but the current fiscal plans of the Italian government are expected to lead to a higher budget deficit. Given very low official estimates of the output gap, the ‘structural’ deficit (2.4%) is estimated to be almost as high as the headline deficit. This model-based estimation implies that the Italian government cannot be expected to meet its medium-term ‘structural’ balance target of 0.5% of GDP; as a consequence, the Commission demands 'corrective' fiscal consolidation measures.

How would alternative output gap estimates affect the Commission’s policy recommendations? Italy would currently run a substantial ‘structural’ budget surplus of 6.3% of GDP if we simply extrapolated pre-crisis potential output growth rates (implying an output gap of -16.5%). Even under the hysteresis scenario, which accounts for the argument that post-crisis potential output growth was much lower, the ‘structural’ budget surplus would amount to 1.8% of GDP.

The implications are clear: alternative estimates of the output gap, which point to a higher degree of resource underutilization against the background of persistently high unemployment, would drastically reduce the fiscal consolidation pressure on the Italian government and point towards the need for expansionary policies that could help to stimulate economic growth and employment. In fact, the report issued by the European Commission would need to look quite different in important respects if it was based on the assessment of higher potential output growth and correspondingly larger output gaps: in this case, the Italian government would overachieve its medium-term budgetary targets, and the Commission’s recommendation for lower government expenditure growth in the face of an allegedly small output gap would turn out to be obsolete.

If the output gap were estimated to be below -4% of GDP, this would matter enormously. The Commission’s own guidelines state that in “exceptionally bad times, interpreted as an output gap below minus 4% of GDP or when real GDP contracts, all Member States, irrespective of their debt levels, would be temporarily exempted from making any fiscal effort.”

Notes: Real GDP and potential output in billion € at constant 2000 prices. Budget balance and structural budget balance in % of GDP. Data: AMECO (Spring 2019 update); own calculations.

Other countries are also affected by output gap estimation problems

Italy’s loss in potential output in 2019 amounted to 16.7% (in relation to the growth trend in pre-crisis years). Germany, however, records a potential output gain of 0.4%. As the figure below shows, the correlation between changes in potential output and changes in actual output (calculated in relation to the pre-crisis trend) is strongly positive for the group of euro area countries.

Over the last ten years, downward revisions in potential output increased fiscal consolidation pressures, because they pointed to higher ‘structural’ deficits. Due to their institutionalization in the EU’s fiscal rules, higher ‘structural’ deficits required stronger fiscal consolidation efforts when it comes to meeting medium-term budgetary targets. Furthermore, low output gap estimates indicated to economic policy-makers that there was in general not much room to use expansionary policies to stimulate the economy. As a consequence, low growth rates and high unemployment are increasingly considered to be 'normal'.

Overall, estimations of high “structural” deficits support the dominant political narrative, according to which “excessive” budget deficits are the root cause of existing macroeconomic problems. The implicit imperative of the European Commission’s output gap model in crisis times is 'more fiscal austerity' – which directly results from the pro-cyclical estimates of potential output. The catastrophic aspect of this imperative is that those countries that implemented the harshest fiscal austerity measures from 2010 onwards also experienced a more severe crisis – and those countries with smaller fiscal consolidation efforts managed to perform much better in relative terms.

Over the period 2010-2019, the imperative of additional fiscal austerity was not only relevant for Italy; other countries, such as Spain, where the unemployment rate still stands above 14%, were also hit hard. The strong positive correlation between actual and potential output losses in the figure above suggests that the “normalization” of the crisis based on low output gap estimates for countries such as Italy and Spain is a direct consequence of the Commission’s pro-cyclical model estimates. It is therefore not surprising that several EU member states, including Italy and Spain, have criticized and challenged the Commission’s potential output calculations by pointing to their apparent lack of macroeconomic plausibility.

The danger of an escalating crisis

Former Italian governments were in a similar situation as the current coalition government consisting of the Lega and the Five Star Movement: controversial output gap estimates and their implications in the EU fiscal regulation framework systematically reduced their scope for conducting fiscal policy at the national level. As a consequence, fiscal policy was largely unable to support economic recovery, and the persistent slump worsened the outlook for improving public debt sustainability.

By criticizing 'the failure of the EU’s fiscal rules', Salvini has consistently attacked European institutions on budgetary matters. Italy’s right-wing populists are highly successful when it comes to making Italian voters believe that the EU deserves to be blamed for virtually all problems in the Italian economy. One indication of Lega’s success is that they won the EU parliamentary elections by a wide margin.

It would be a grave mistake if the European Commission and the EU’s finance ministers decided not to take the Italian government’s criticism of the EU’s fiscal rules seriously. If the output gap in the Italian economy were more negative (implying higher underutilization of economic resources), expansionary policies could and should indeed be used to stimulate growth and employment in Italy. A critical discussion of the Italian government’s plans for tax cuts and spending increases are certainly required. For example, the Commission could question whether tax cuts are the most effective measure to stimulate the economy and ensure debt sustainability: based on the existing evidence, increases in public investment should be expected to be more effective in stimulating growth, while permanent tax cuts would lower the long-term revenue base. But instead of promoting an evidence-based discussion with the Italian government about the most sensible fiscal policies, the European Commission has decided to insist on further fiscal consolidation measures, which – given the experience of recent years – will not provide a solution to Italy’s most pressing problems.

The right dose of fiscal stimulus might be just what the Italian economy needs in the short-term, as Ashoka Mody has pointed out. Policy discussions should be evidence-based and focus on how to achieve good fiscal policy outcomes. In this context, it is high time to acknowledge that the one-sided focus on deficit and debt reduction within the EU fiscal regulation framework has been largely counterproductive, making it more difficult for Italy (and other countries) to find solutions for its macroeconomic problems and leading to a further increase in the real debt burden. Italian governments ran substantial primary budget surpluses over the last ten years (actually, they have been doing so since the mid-1990s), which shows that significant fiscal consolidation efforts were indeed undertaken. But the public-debt-to-GDP-ratio remains high (at more than 130% of GDP) as economic growth continues to falter.

The hard stance of the European Commission and the majority of EU government heads and finance ministers vis-à-vis the Italian government is not only shortsighted from an economic point of view. It is also a very dangerous political game, because the standoff leads to additional uncertainties on government bond markets, which could lead to further increases on Italy’s government bond yields, leading to an escalation of the economic and political crisis. If the Italian government decides not to back down, there might be an escalation in terms of a broader eurozone crisis, which would pose a threat to the eurozone in general.

What is the restrictive stance good for, anyway? Is precise compliance something to be valued in itself? Does it make sense to insist on ensuring the “credibility” of a set of rules that has been criticized repeatedly and consistently by different economists and experts, as these rules have been shown to lead to bad macroeconomic outcomes, especially in times of crisis? If the goal of European policy-makers was to calm down the situation on government bond markets, it would arguably be much more important to work on a policy strategy that promises to put the Italian economy on a sustainable path of economic recovery. In fact, doubling-down on fiscal consolidation requirements will simply not support the recovery. At the same time, there would still be enough “flexibility” when it comes to interpreting Italy’s fiscal rule compliance, as indicated by experiences from the recent and less recent past.

An alternative way forward

Quite obviously, it would be equally shortsighted to believe that a bit more room for expansionary policies will solve Italy’s actual structural problems (such as the oversized banking sector with lots of bad assets, dysfunctional elements in its political system, the economic divide between Northern and Southern Italy, low productivity growth and an export sector that has partly fallen behind in terms of technological competitiveness). However, if European policy-makers were to understand that it is counterproductive to be overly restrictive in Italian budget affairs, there would be more hope to see a policy stance that can actually support economic growth, bring down unemployment and curb deflationary pressures, which would also help to ease existing debt problems.

The Italian economy has to overcome its quasi-permanent slump, which would also make it easier to address existing structural problems. In particular, targeted industrial policies would be required to improve production structures and to allow Italian firms to gain technological competitiveness in crucial sectors. Additional fiscal consolidation measures and labor market deregulation, based on the European policy-makers’ favorite post-crisis recipes, would serve to lengthen the slump.

Controversial technocratic assessments based on the output gap are deeply engrained in the European Commission and other European institutions. Over the last years, these model-based assessments have served to 'normalize' low growth and high unemployment rates in Italy and several other euro area countries – without delivering any convincing economic policy perspective about how to actually overcome the crisis. Recent surveys suggest that a majority of the Italian population does not trust the EU. The insistence of the European Commission and EU finance ministers on a path of fiscal consolidation inconsistent with economic recovery and a declining real debt burden will not convince Italian voters to trust European institutions.

A continuation of the 'No'-stance vis-à-vis the Italian government in budgetary matters is indeed likely to help right-wing populists to continue to successfully campaign against Italy’s membership in the euro area and the EU. If EU policy-makers want to avoid deep cracks in the euro area after an exit of Italy, they will need to talk straight on the importance of seemingly merely technical, but eventually politically relevant estimations of the output gap. This should be brought to the attention of the European public and lead to discussions about how to change the course of European economic policy.

Note: Translated and adapted from an article that first appeared in Makronom. The original article is here (in German).