Italy is of systemic importance – European solutions are needed

10 April 2020

The Italian economy has been in a kind of smouldering permanent crisis, but the negative economic effects of the Corona shock have worsened it.

By Philipp Heimberger

photo: iStock.com/Em Campos

- Because Italy is of systemic importance, the developments there will also put the euro area as a whole to the acid test once again.

- Those who want to prevent the collapse of the euro must participate in common European solutions that create a credible perspective of positive economic development in the south of the euro area for the period after the lockdown.

- The results achieved by the finance ministers in this week’s Eurogroup meetings leave crucial questions about burden sharing of the crisis costs unanswered. They vaguely promise a “recovery fund”, but it remains unclear how big this fund will be and how it can be financed.

When Italy emerges from the Corona health crisis, it will face an enormous challenge of economic recovery. However, Italy's ability to bear the costs of fighting the crisis and of the measures that will soon be needed to revive the economy is limited by legacy debt; successful crisis management will therefore depend to a large extent on the credibility of mutual support within the euro area.

The ECB is already making a decisive contribution: it is buying up government bonds on a large scale under the PEPP ("Pandemic Emergency Purchase Programme"). As a result, risk premiums on Italian government bonds, which had already risen dangerously a few weeks ago, have fallen again. The PEPP program is thus currently ensuring that the Italian government can continue to refinance itself at very low cost during the corona crisis.

However, a key issue remains largely ignored in the north of the euro area: On its own, Italy will not be able to get the economy back on track after the Corona lockdown. Although Italy is probably in the most difficult situation and therefore represents the "fault line" for the future of the euro area, other countries hard hit by the crisis, such as Spain, will hardly be able to get through with solely national efforts.

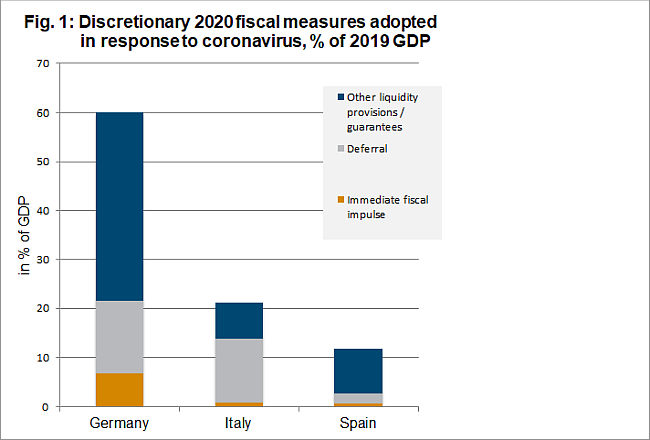

There is a real danger that Italy, like some other countries, will only be able to finance the most urgent measures, while countries with a better starting position - such as Germany, Austria or the Netherlands - will have more fiscal space to support a rapid recovery once the lockdown is over. The difference in fiscal responses to the corona crisis already clearly shows this: according to calculations by the think tank Bruegel, the immediate fiscal impulse for Germany (in the form of additional government spending on medical equipment, short-time work, subsidies for small and medium-sized enterprises, etc.) amounts to around 7% of economic output in 2020, compared with only 0.9% for Italy. And Italy's response so far also lags behind Germany in terms of deferral of taxes and social security contributions as well as other liquidity provisions and loan guarantees.

A continued highly divergent fiscal policy response by member states would result in an uneven recovery from the corona crisis and a political dynamic that could lead to the collapse of the euro area. The painful memories of the euro crisis should actually still be fresh: When the countries on the euro periphery implemented tough fiscal austerity measures after the financial crisis, this hit their economies hard, which paradoxically exacerbated their sovereign debt problems and led to politically toxic creditor-debtor conflicts.

Source: Bruegel

The package of measures negotiated this week in the Eurogroup still leaves longer-term questions about burden sharing in the Corona crisis unresolved. The finance ministers agreed at the last meeting on a package of 500 billion euros to alleviate the crisis. An ESM credit line will be established (up to 240 billion euros), which, although only subject to minor conditionality, will be limited to covering "direct and indirect" health costs. However, government spending on healthcare costs will not play a major role in the big picture of the costs of the crisis, especially since it is doubtful whether a country like Italy would ever use such a credit line under the existing conditions. In addition, there will be a EU programme to grant member states cheap loans without conditions to support short-time work, which is called SURE (Support to Mitigate Unemployment Risks in an Emergency). This will enable the EU to borrow on the markets and to pass on the funds to the member states. Furthermore, there will be loan guarantees from the European Investment Bank for companies.

But finance ministers have still done nothing concrete to end the dispute over how to finance longer-term efforts to revive the economy across the euro area after the crisis. While there is agreement on the creation of a "recovery fund", there is still no agreement on the important details. At the very least, decision-makers are admitting that the package of measures put together so far will not be sufficient. But how large the recovery fund is to be and how the burden sharing can work in practice remains completely unclear. According to the agreement, the finance ministers are to find "innovative financial instruments" for the recovery fund, which, however, can be understood to mean different things: Dutch Finance Minister Hoekstra says that "innovative financial instruments" is “deliberately vague” so that all stides can read what they want into it. Italy and some other countries, on the other hand, continue to insist that burden-sharing of the costs of the crisis should be achieved through common debt instruments.

The question of how to open up a credible perspective of positive economic development for the coming years, especially for Italy, but also for Spain and other countries particularly hard hit by the crisis, is central to the future of the Eurozone. However, the necessary complement to the ECB's PEPP programme by a strong European fiscal policy response remains outstanding even after the recent Eurogroup meeting.

Italy's crisis in a broader context

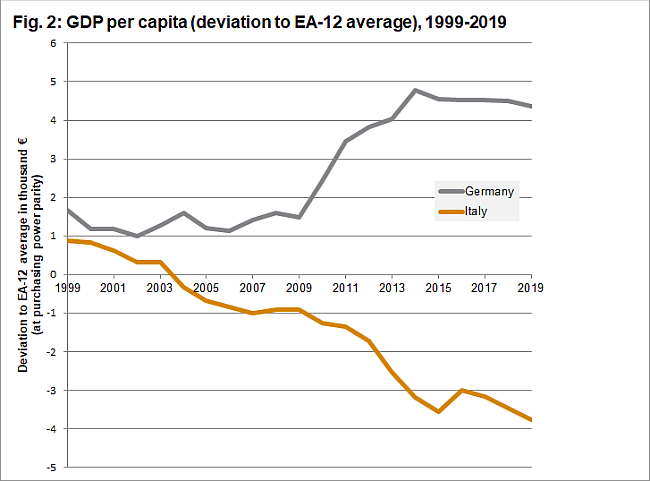

Italy's currently precarious situation can be better understood in a broader context: For years, the Italian economy has been in a kind of smouldering permanent crisis, which is dramatically aggravated by the negative economic effects of the Corona crisis. While per capita GDP (in purchasing power parities) in Italy in 1999 was still around €1000 above the Euro area average, twenty years later - just before the corona crisis began - it had fallen almost €4000 below the Euro area average. Germany, on the other hand, where per capita incomes were already slightly higher than in Italy when it joined the euro, continued to chip away over the same period, resulting in an increasing GDP per capita gap.

Data: Eurostat; own calculations. Euro area average (EA-12) includes the following countries: Austria, Belgium, Germany, Spain, Finland, France, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal.

Thus Italy had already lost two decades in its economic development before the corona crisis. The political promise that came with the introduction of the euro as the peak of the process of economic integration in Europe remains unfulfilled: when the euro area was created, policymakers had promised that, thanks to economic integration into the European currency area, the southern euro countries would, in the long term, move closer to the higher level of prosperity of richer countries such as Germany and Austria. However, the experience with the common European currency area before the Corona crisis clearly contradicts this political promise. (The structural polarization between core countries such as Germany and peripheral countries such as Italy, which underlies this macroeconomic divergence, has been analysed by my colleagues Gräbner, Kapeller, Schütz and myself in an article recently published in the Cambridge Journal of Economics).

Public legacy debt and fiscal austerity

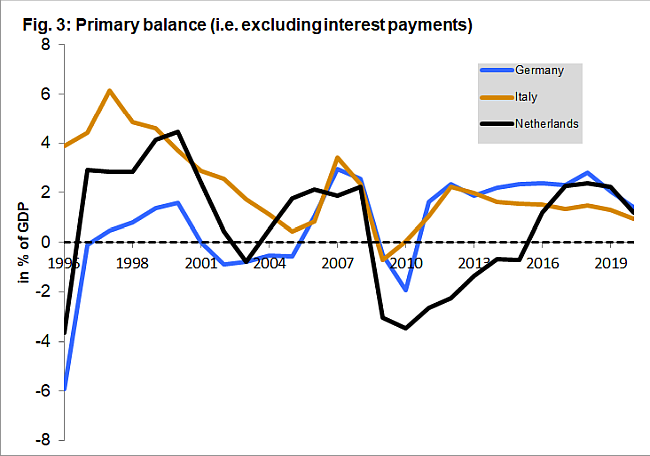

The high level of Italian public debt is due to legacy debt from the 1980s and 1990s. Since the mid-1990s, however, the various Italian governments have made considerable efforts to reduce the debt burden, even if this is usually ignored in the media: Since 1995, the Italian government has achieved a substantial primary surplus almost continuously; in other words: excluding interest payments, government revenue has exceeded government expenditures. Since 1995, the Italian state has posted a primary surplus in 24 out of 25 years; the crisis year 2009 was the only exception so far. Due to the fiscal consolidation measures implemented since the financial and economic crisis, Italy achieved primary surpluses even in the years before the corona crisis despite weak growth and declining tax revenues. However, despite these primary surpluses, the public debt ratio could only be stabilised at around 130% of GDP.

Data: AMECO (Autumn 2019)

Since the introduction of the euro, Germany, Austria and the Netherlands have had significantly lower and less sustained primary surpluses than Italy. Nevertheless, in these three countries one narrative still dominates public discourse, namely that the Italians are to blame themselves if they can do less to support their economy in the current situation than the northern euro countries. Dutch finance minister Hoekstra had caused indignation in the southern euro countries when he suggested that the EU Commission should investigate why Italy and other southern countries did not have sufficient fiscal space to combat an economic downturn. Apart from the fact that Hoekstra and others have made a mockery of a European spirit of solidarity, thereby disappointing the crisis-stricken population in Italy and other countries, this attitude is untenable in terms of content - especially when it comes to Italy: no other country has so consistently run up primary surpluses since the introduction of the euro.

Of course, in addition to the high public debt ratio, the Italian economy also has considerable structural problems: the ailing banking sector, which is far too large, holds many bad loans and has cost taxpayers many billions in recent years as a result of repeated state bailouts; weak productivity growth over recent decades; dysfunctional elements of the political system; the economic polarisation between northern and southern Italy; problematic developments in the Italian industrial sector, etc. However, Italy's persistent aggregate demand and productivity misery is also a consequence of the shortcomings of the institutions and rules in the Euro area. While Italy has not been able to pursue a tailor-made monetary and exchange rate policy to support economic development since joining the euro, the restrictive European fiscal rules and austerity requirements of the EU Commission (and the ECB) have also systematically tied the hands of national fiscal policy in the years before the Corona crisis – based on controversial technocratic assessments.

Negative developments of aggregate demand, exacerbated by fiscal consolidation pressures, have plunged the Italian economy into a quasi-permanent smouldering crisis in the years before Corona: while the German economy grew by an average of 2.0% in real terms and the euro area by 1.4% per year over 2010-2019, real GDP growth in Italy was only 0.2% in the same period – apparently to the complete surprise of institutions such as the IMF and the EU Commission, which for years systematically underestimated the negative growth effects and of fiscal consolidation measures.

Italy is of systemic importance

In the wake of the Corona crisis, Italy's public debt ratio will rise sharply once again. However, it would have disastrous consequences for the Italian economy and the sustainability of the debt if, soon after the peak of the Corona health crisis, European policymakers were to press for further strict austerity measures in the Italian national budget - and the political price could be even higher.

Matteo Salvini and other right-wing populists will take advantage of any undecidedness and shortcomings in the European response to the Corona crisis to stir up sentiment against the European institutions. In a survey conducted at the beginning of last month, 88% of Italians interviewed already said that they felt that Europe did not support Italy and a staggering 67% reported that they saw EU membership as a disadvantage. "Is Europe losing Italy?" was the title of a recent article in the Financial Times.

But an Italian exit from the euro area (and possibly even from the EU) would have significant negative consequences not only for Italy: The reintroduced lira would initially depreciate sharply, making imported goods more expensive and further increasing unemployment. An Italian public debt bankruptcy would hardly be avoidable if the national currency were reintroduced, because the euro-denominated debt would be overwhelmingly high in the event of sharp currency devaluation. Italy's gross public debt currently stands at just under €2,500 billion - a multiple of Greece's public debt of around €330 billion - but it will rise considerably again in the wake of the Corona crisis. Italy has Europe's third-largest banking sector, which holds a high proportion of Italian government bonds.

In other words: Italy is systemically important, and Italian turbulence would lead to rippling effects in the European and global financial systems, which would also trigger a further decline in economic activity in the euro area, which has already been severely affected by the corona crisis. Euro area countries such as Germany, the Netherlands and Austria should be interested in doing “whatever it takes” to avoid such an outcome. This means that these countries should not afford to look the other way or pretend that Italy can cope with the emerging macroeconomic problems resulting from the corona crisis in Italy.

Offering a perspective of positive economic development to save the euro

In order to ensure the long-term sustainability of Italian public debt even after the corona crisis and to guarantee the cohesion of the euro area, a convincing perspective of positive economic development for the period after the corona lockdown is needed. Such a perspective would have to be clearly communicated by the European decision-makers in order to get the population of Italy back on board in other countries that were hard hit by the crisis, and thus reduce the foreseeable rise in popularity of Eurosceptic parties. The Spanish Prime Minister Sanchez, for example, recently called for a "new Marshall Plan" for Europe, which would also have to provide for extensive public investment.

Debates have come to a head in recent weeks over "Coronabonds": nine euro area countries jointly called for the (one-off) issuance of common bonds to co-finance the fight the crisis. The rejection of this demand by Germany, the Netherlands, Austria and Finland is hardly surprising in view of the continuing lines of conflict from times of euro crisis ("moral hazard", "no joint debt liability"). However, the brusque nature of the rejection, coupled with a publicly displayed lack of interest in the difficult situation in countries such as Italy and Spain on the part of central decision-makers like the Dutch Finance Minister Hoekstra, was anything but helpful. This is one of the reasons why the mood in Italy seems to have been tilted, even among thousands of people who used to think positively of the common European institutions.

Italy, but probably also other countries that have been badly hit, such as Spain, will simply not have the necessary national leeway to fight the crisis and to promote economic recovery. A European support mechanism is therefore urgently needed. With the "recovery fund" promised at the Eurogroup meeting, the EU would need to be enabled to raise hundreds of billions of euros on the capital markets. This requires new instruments, but there are also proposals that do not require the joint liability the Netherlands and Germany are so vehemently opposed to. Grund, Guttenberg and Odendahl propose, for example, the establishment of a European fund backed by guarantees from the Member States, but liability would remain with the EU.

This article has shown that the Italian economy was already in a kind of smouldering permanent crisis in the years before the Corona crisis. Given that this crisis has drastically worsened due to the Corona shock, hoping that relatively small-scale economic policy initiatives will suffice to keep the euro area together in the post-corona lockdown period is a dangerous game to play, and could still also cause very great damage to the populations of the core countries of the euro area. If the crisis in Italy (and some other member states such as Spain) is to be successfully overcome and the survival of the euro secured, European decision-makers will have to that burden-sharing of costs over a longer period of time is needed to open up a credible perspective of positive economic development after the peak of the corona health crisis. Once a consensus on this point can be reached at European level, no technical problem of implementation will appear insurmountable.