Unemployment in Europe: What should be done?

13 May 2019

Stable labour market institutions, public investment programmes and active labour market policies are essential for reducing high unemployment rates in several European countries.

- In many European countries, unemployment remains higher than it was before the beginning of the financial and economic crisis about ten years ago.

- However, with consistent welfare-oriented economic policies, a significant improvement of the situation could be achieved at both the national and European level.

- These policies would have to be based above all on a public investment offensive and an active labour market policy. This could reduce the unacceptably high level of unemployment.

The evolution of unemployment in Europe

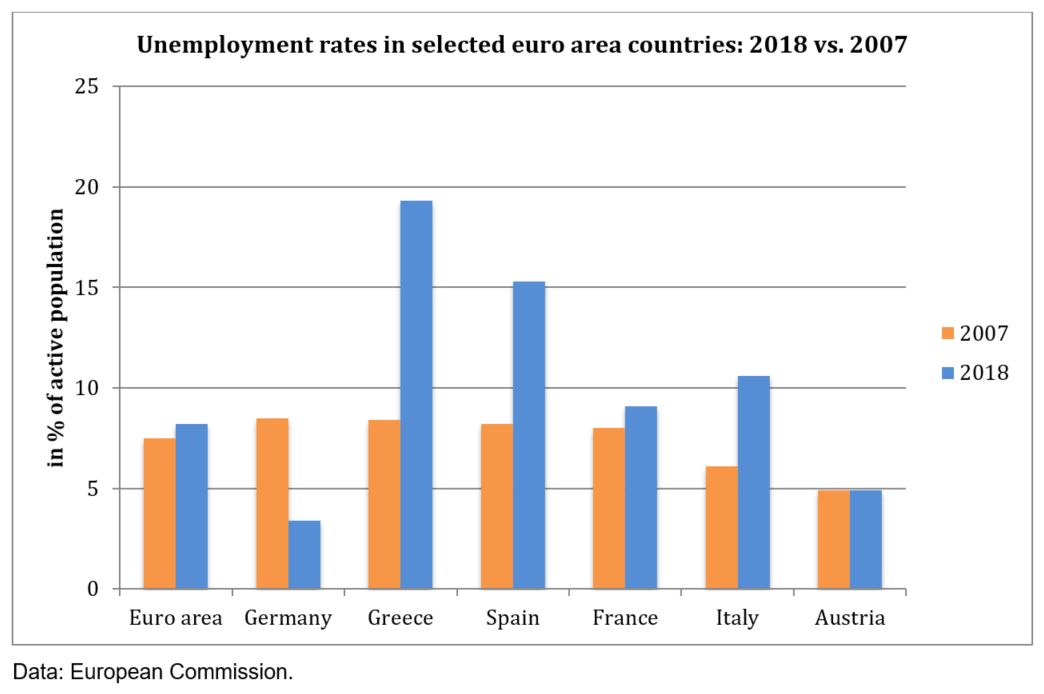

The financial and economic crisis of 2008-2009 led to a marked rise in unemployment in Europe. In the euro area, the unemployment rate rose from 7.5% in 2007 to 12% in 2013; by 2018 it still amounted to as much as 8.2%, as shown by Figure 1. Unemployment in the euro area is therefore currently still higher than it was before the crisis began some ten years ago. According to official Eurostat statistics, 11.6 million people were unemployed in the euro area in September 2008; most recently that number was 12.8 million people – i.e. still around 1.2 million more than in the pre-crisis period.

Although there was a prolonged economic upswing over much of 2017-2018, the problem of unemployment remains acute and should be tackled urgently by policy-makers. Of course, the problems are unevenly distributed across the European countries, as the Southern European countries most affected by the crisis and the austerity policies continue to face the biggest labour market challenges. Deviations from the full employment target are all the more problematic because the outlook for the eurozone economy is already deteriorating against a background of rising global risks, although some of the negative sentiment could eventually also prove overdone.

Labour market flexibilisation has exacerbated the crisis in many EU countries

Why is unemployment in many European countries still at elevated levels compared with the pre-crisis period? This question is of crucial importance from an economic policy point of view. In recent years, numerous international institutions and leading economic policymakers at the European level have emphasised the importance of structural and institutional factors. Unemployment is said to be relatively high in large parts of Europe because the crisis has allegedly shown that labour market institutions are too ‘rigid’. Those taking this view emphasise what they see as excessively high minimum wages and unemployment benefits, strict employment protection regulations, high tax burdens for companies, and a distorting influence of trade unions. In short, high unemployment is considered to be generally due to high ‘structural’ unemployment. According to this perspective, expansionary economic policy measures – for example the creation of employment through public infrastructure projects – could at best contribute only marginally to solving this problem.

The dominant view in European economic policy over the last ten years has been that by reducing minimum wages and unemployment benefits and by making it easier for companies to hire and fire workers, the unemployment problem would solve itself. Policymakers expected that measures such as cuts in unemployment benefits, dismantling employment protection regulations, and the weakening of trade unions through decentralisation of the wage bargaining system, would eliminate ‘labour market rigidities’ that allegedly stand in the way of a reduction in unemployment. In their practical implementation, ‘structural reforms’ have been clearly lop-sided in favour of reducing workers’ rights and the labour market institutions protecting those rights. Proponents of such ‘structural reforms’ argue that, first, these reforms would increase incentives for the unemployed to accept low-paid jobs and increase their work effort. Second, in the supply-side model of some economists, the ‘structural reforms’ have an expansionary effect on economic growth and employment as the production costs of enterprises fall.

A record of failure

Within Europe, Southern European countries in particular have had to implement comprehensive deregulation measures in their labour markets over the past decade. Although the academic debate is much more nuanced, the biased story about the allegedly very positive economic impact of labour market deregulation has been dominating the media discourse for decades. However, empirical evidence points to the fact that – in stark contrast to conventional expectations – the flexibilisation of labour market institutions did not lead to falling unemployment. Instead, it led to considerable reductions in wages, which exacerbated the crisis by reducing aggregate demand. Figure 2 shows that, for the particularly relevant eurozone crisis period 2010-2014, there is a very close correlation between the development of real wages and the change in the unemployment rate for the eurozone countries. In the countries with the strongest downward wage pressure, the unemployment rate rose most markedly; conversely, the development of the unemployment rate was more favourable in those countries where real wages increased. The largest wage losses were recorded in the Southern European countries, which were most affected by labour market deregulation.

What role for protective labour market institutions?

One strand in the relevant literature argues that labour market institutions can be very helpful in stabilising economic expectations. This is because they provide security for working people (e.g. employment protection regulations) and safeguard their income levels, both in periods of employment and unemployment (through minimum wages or unemployment benefits). Such a stabilisation of expectations can in turn promote innovation and labour productivity and stimulate consumer demand, while labour market institutions can also contribute to a stable macroeconomic development. Therefore, the idea that protective labour market institutions generally lead to inefficient market distortions and should therefore be reduced (a view that often dominates the economic policy debate), is thus fundamentally called into question.

What factors explain unemployment over time?

Building on the factors outlined in the previous two paragraphs, my current research provides empirical evidence that the development of unemployment rates in a more historical perspective (from the mid-1980s to 2013) in a group of developed economies (including Austria) cannot be explained primarily by institutional labour market factors. Indeed, standard labour market variables – such as employment protection, unemployment benefits, minimum wages, trade union density and the tax wedge – largely underperform when it comes to explaining unemployment. Even if one accepts the questionable methodology used by the European Commission to break down the unemployment rate into a cyclical component (determined by the ups and downs of the business cycle) and a ‘structural’ component (theoretically determined by institutional labour market factors), it also appears that the development of the ‘structural’ part of the unemployment rate is not systematically related to institutional labour market factors.

Macroeconomic factors are central to explaining unemployment

A central finding of recent research is that capital accumulation – defined as the ratio of gross fixed capital formation to the net capital stock, which measures rates of change of the capital stock – is a robustly significant and economically relevant determinant of the unemployment rate. Although labour market institutions may have some influence on unemployment in developed economies, this influence appears to be much smaller than the influence of macroeconomic variables such as capital accumulation and the real long-term interest rate. In particular, as capital accumulation increases, unemployment decreases (and vice versa). My research shows that this result is very robust.

Increases in unemployment cannot simply be explained by an allegedly distorting influence of protective labour market institutions. Empirical evidence suggests that deregulating labour markets – by cutting unemployment benefits and minimum wages, decentralising wage bargaining, etc. – is not the solution to the problem of increased unemployment in much of Europe. However, as higher capital accumulation is robustly linked to lower unemployment, it can be concluded that stimulating investment should be high up on the agenda of economic policy-makers seeking to reduce unemployment.

Policy implications: everyone would win from higher public investment

The above evidence indicates that economic policy could significantly contribute to preventing the persistence of unacceptably high unemployment rates. Public initiatives that boost investment and lead to an increase in the (public) capital stock could be of particular importance. In the current environment of very low interest rates, higher public investment would not only be an effective employment policy, but would also create incentives for private companies to invest more. In addition, public investment could be used to target key societal challenges such as climate change, the ageing of the population and digitisation.

More public investment is meaningful and necessary under the given conditions in Europe. In order to allow more public investment in those areas that are particularly relevant for economic and social development, the EU budget rules should also be amended. This could be achieved, for example, by introducing a ‘golden investment rule’ that excludes deficit-financed increases in the public capital stock (e.g. by investing in social, ecological and digital infrastructure) from the relevant deficit calculation.

In addition to these fundamental considerations regarding the longer-term role of public investment for improving the capital stock, economic policy should focus on preparing economic stimulus packages in view of the current weakening of economic growth rates in large parts of the euro area. Moreover, targeted active labour market policies for at-risk groups (in particular, older long-term unemployed and young people with inadequate qualifications) could help to effectively address the problem of unemployment.